A repossession stays on your credit report for seven years from the date of first delinquency, not from the date your vehicle was taken. During that time, a repo can lower your credit score by 100 to 150 points or more. The good news: you can take steps right now to dispute inaccurate repo entries, negotiate with lenders, and rebuild your credit faster than you think.

Dealing with a repossession on your credit report?

M1 Credit Solutions uses AI to analyze your credit report, identify errors in repo entries, and generate customized dispute letters in minutes.

If you have ever walked outside to find your car missing, or if you are struggling to keep up with auto loan payments, understanding how long a repo stays on your credit is the first step toward taking control of your financial future.

In this guide, we will cover exactly how repossession affects your credit report, the real difference between voluntary and involuntary repo, proven strategies for getting a repo removed early, and step-by-step methods for rebuilding your credit score after repossession.

What Is a Repossession and How Does It Appear on Your Credit Report?

A repossession happens when a lender reclaims a financed asset, most commonly a vehicle, because the borrower has defaulted on the loan agreement. When you finance a car, the vehicle serves as collateral. If you fall behind on payments, typically by 90 days or more, the lender has the legal right to take the vehicle back.

On your credit report, a repossession does not appear as a single entry. It triggers a chain of negative marks that can include:

- Late payments recorded for each month you missed before the repo

- Account default showing the loan was not repaid as agreed

- Repossession or voluntary surrender status on the auto loan account

- Charge-off if the lender writes the debt off as a loss

- Collection account if the remaining balance is sold to a debt collector

Each of these items compounds the damage to your credit profile. Understanding what appears on your report is essential before you can take action to fix it.

How to Check Your Credit Report for Repo Entries

You can obtain free copies of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. Look for accounts marked with statuses like “Repossession,” “Voluntary Surrender,” or “Charged Off” under your auto loan accounts.

With M1 Credit Solutions, you can connect your credit reports from all three bureaus and our AI platform will automatically identify repossession entries, late payments, and other negative items that are dragging your score down.

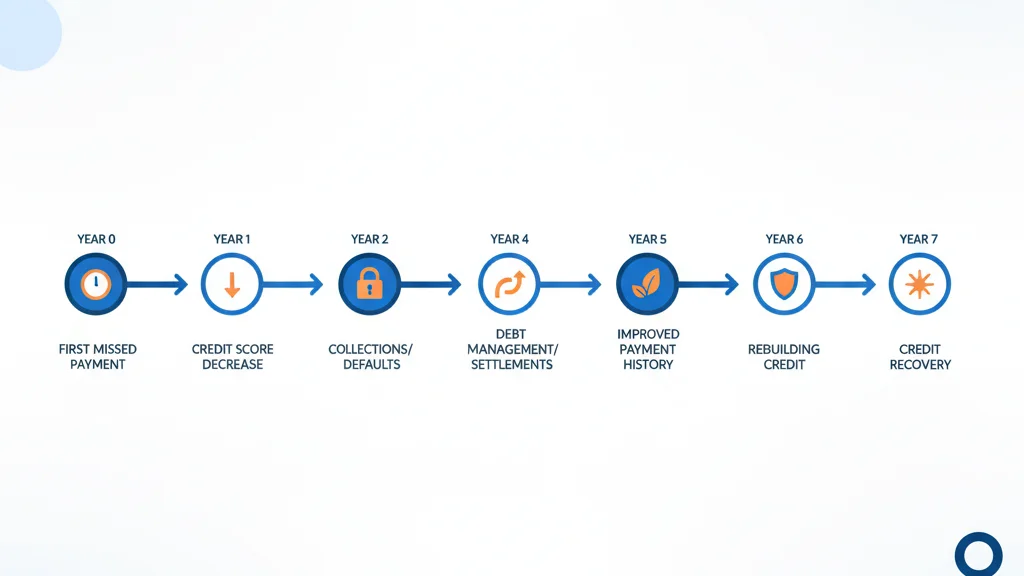

How Long Does a Repo Stay on Your Credit Report?

A repossession stays on your credit report for seven years from the date of first delinquency. This is a critical distinction that many people misunderstand.

The clock does not start from:

- The day your car was physically repossessed

- The date you voluntarily surrendered the vehicle

- The day you received a deficiency balance notice

- The date the account went to collections

The seven-year countdown begins on the date of first delinquency, which is the first missed payment after which the account was never brought current again.

Example Timeline

Imagine you miss your first auto loan payment in January 2026. You never catch up, and your car is repossessed in April 2026. Even though the repossession happened in April, the seven-year clock started in January 2026. The repo will be removed from your credit report in January 2033.

This distinction matters because some lenders and collection agencies may report incorrect dates, which can extend the time a repo stays on your report. If you notice a discrepancy, you have the right to dispute the error on your credit report.

What Happens After the 7-Year Period?

Once seven years have passed from the date of first delinquency, the repossession and all associated negative entries (late payments, charge-offs, collection accounts tied to that repo) should automatically fall off your credit report. If they do not, you can file a dispute with the credit bureaus to have them removed.

How Much Does a Repossession Hurt Your Credit Score?

A repossession is one of the most damaging events that can appear on a credit report. The impact depends on your credit profile before the repo, but here is what you can generally expect:

| Credit Score Before Repo | Estimated Score Drop | Recovery Timeline |

|---|---|---|

| 750+ (Excellent) | 150-200+ points | 3-5 years with active rebuilding |

| 680-749 (Good) | 100-150 points | 2-4 years with active rebuilding |

| 580-679 (Fair) | 80-130 points | 1-3 years with active rebuilding |

| Below 580 (Poor) | 50-100 points | 1-2 years with active rebuilding |

People with higher credit scores typically experience a larger point drop because they have more to lose. However, regardless of where you start, the damage from a repo decreases over time. The most severe impact occurs in the first one to two years, then gradually lessens as the entry ages.

The Compound Effect of Repo-Related Entries

A repossession rarely appears as a single negative item. The cascade of related entries, including late payments, default status, charge-off, and potential collection account, creates a compounding negative effect. Each individual item drags your score down, and together they can make it difficult to:

- Get approved for new auto loans or credit cards

- Qualify for a mortgage or apartment rental

- Secure favorable interest rates on any credit product

- Pass employment background checks in some industries

This is exactly why taking action to fix your credit score as soon as possible after a repossession is so important.

Voluntary vs. Involuntary Repossession: Does It Matter?

Many people assume that voluntarily surrendering a vehicle looks better on their credit report than having it forcibly repossessed. The reality is more nuanced than that.

Involuntary Repossession

This is the traditional repo scenario. The lender sends a repossession agent to physically take the vehicle, often without warning. On your credit report, it appears as “Repossession” and signals that the borrower did not cooperate with the lender.

Voluntary Surrender

Also called “voluntary repossession,” this happens when you proactively return the vehicle to the lender because you can no longer afford the payments. On your credit report, it typically appears as “Voluntary Surrender.”

The Credit Impact Is Similar

Here is the hard truth: both types of repossession damage your credit in nearly the same way. Credit scoring models like FICO and VantageScore treat voluntary surrender and involuntary repossession similarly because both indicate a failure to repay the loan as agreed.

However, voluntary surrender does offer some practical advantages:

- Lower fees: You avoid repossession fees (typically $300-$500) that get added to your deficiency balance

- Better lender relationship: Some lenders may be more willing to negotiate on the remaining balance

- Potentially faster resolution: You avoid the uncertainty and stress of waiting for the repo agent

- Legal protection: In some states, voluntary surrender may offer additional consumer protections

If you are facing the possibility of repossession, contact your lender immediately. You may be able to negotiate a loan modification, deferment, or payment plan that avoids repossession entirely.

How to Get a Repo Off Your Credit Report

While a repossession is designed to stay on your credit report for seven years, there are legitimate strategies that may result in earlier removal or reduced impact.

1. Review Your Credit Report for Errors

Repossession entries frequently contain reporting errors. Common mistakes include:

- Incorrect date of first delinquency (which can extend the 7-year clock)

- Wrong balance amounts reported to the bureaus

- Duplicate entries from the original lender and a collection agency

- Missing notation that the account has been paid or settled

- Re-aging of the debt (reporting a newer delinquency date than the original)

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any inaccurate information on your credit report. The credit bureaus have 30 days to investigate and respond.

M1 Credit Solutions uses AI technology to scan your credit report and automatically identify these types of errors. Our platform generates customized dispute letters targeting specific inaccuracies, giving you the strongest possible case for removal.

2. Send a Debt Validation Letter

If the repo deficiency balance has been sent to a collection agency, you have the right under the Fair Debt Collection Practices Act (FDCPA) to request debt validation within 30 days of first contact. The collector must provide:

- The original creditor’s name

- The exact amount owed

- Proof that they have the legal right to collect the debt

- Documentation connecting you to the original debt

If the collector cannot validate the debt, they must stop collection activity and remove the entry from your credit report. Learn more about this strategy in our debt validation letter guide.

3. Negotiate a Pay-for-Delete Agreement

A pay-for-delete arrangement is a negotiation strategy where you offer to pay some or all of the remaining deficiency balance in exchange for the creditor or collection agency removing the negative entry from your credit report.

Here is how to approach a pay-for-delete negotiation:

Step 1: Know your leverage. If the debt is several years old, the creditor may be willing to settle for less because the statute of limitations may be approaching.

Step 2: Start with a written offer. Never make pay-for-delete agreements verbally. Send a formal letter proposing the arrangement.

Step 3: Offer a lump sum. Creditors are more likely to agree to pay-for-delete when you can pay the agreed amount immediately.

Step 4: Get the agreement in writing before you pay. This is non-negotiable. Without written confirmation, the creditor has no obligation to remove the entry.

Step 5: Verify removal after payment. Check your credit reports 30-45 days after payment to confirm the entry has been removed.

Not all creditors agree to pay-for-delete arrangements, and the practice exists in a legal gray area. However, smaller collection agencies and original creditors who want to recover some money are often open to negotiation.

4. Dispute Directly with the Credit Bureaus

If you have identified any inaccuracy in the repossession entry, file a formal dispute with each credit bureau reporting the error:

- Experian: experian.com/disputes

- Equifax: equifax.com/credit-dispute

- TransUnion: transunion.com/credit-disputes

Include supporting documentation such as payment records, loan agreements, and correspondence with the lender. The bureau must investigate within 30 days and either verify, correct, or delete the disputed information.

5. Use AI-Powered Dispute Tools

Manual dispute processes can be time-consuming and overwhelming, especially when dealing with multiple negative entries from a single repossession. M1 Credit Solutions streamlines this process by:

- Connecting to your credit reports from all three bureaus

- Using AI to identify every disputable error in your repo entries

- Generating legally sound, customized dispute letters

- Tracking dispute progress through a real-time dashboard

- Suggesting the most effective dispute strategy for your specific situation

Start your free credit analysis to see what negative items on your report may qualify for dispute.

Rebuilding Your Credit After a Repossession

Whether you successfully remove the repo from your credit report or need to wait out the seven-year period, actively rebuilding your credit is essential. Here are proven strategies that work:

Make Every Payment on Time

Payment history accounts for approximately 35% of your FICO score, making it the single most influential factor. After a repossession, every on-time payment you make demonstrates to future lenders that you have changed your financial behavior.

Set up automatic payments for every bill and credit account to ensure you never miss a due date.

Lower Your Credit Utilization

Credit utilization, or the percentage of available revolving credit you are using, makes up about 30% of your score. Keep your credit card balances below 30% of their limits, and ideally below 10% for the fastest score improvement.

Consider a Secured Credit Card

A secured credit card requires a cash deposit that serves as your credit limit. It is one of the most reliable tools for rebuilding credit after a negative event like repossession. Use it for small, recurring purchases and pay the balance in full each month.

Become an Authorized User

If a trusted family member or friend has a credit card with a long history of on-time payments and low utilization, ask to be added as an authorized user. Their positive payment history may be reported on your credit file, giving your score a boost.

Monitor Your Credit Regularly

Tracking your credit score and report helps you measure progress and catch any new errors quickly. With M1 Credit Solutions, you can monitor all three bureau reports from a single dashboard and receive alerts when changes occur.

Avoid New Hard Inquiries

Each time you apply for credit, a hard inquiry appears on your report and can temporarily lower your score by a few points. After a repossession, be strategic about new credit applications. Only apply when you have a reasonable chance of approval.

Frequently Asked Questions About Repossession and Credit

How long does a repo stay on your credit if you pay it off?

Paying off the remaining balance after a repossession does not remove the repo from your credit report. It will still remain for seven years from the date of first delinquency. However, the account status will update to “Paid” or “Settled,” which looks better to future lenders than an unpaid repo. You may also negotiate a pay-for-delete arrangement where the creditor agrees to remove the entry in exchange for payment.

Can a repossession be removed from your credit report before 7 years?

Yes, in certain circumstances. If the repossession entry contains inaccurate information, you can dispute it with the credit bureaus and have it removed. You can also negotiate a pay-for-delete agreement with the creditor. Additionally, if the creditor or collection agency cannot validate the debt when challenged, the entry must be removed. M1 Credit Solutions uses AI to identify errors in repo entries that may qualify for early removal.

Does voluntary repossession hurt your credit less than involuntary?

Both voluntary surrender and involuntary repossession have a similar negative impact on your credit score. Credit scoring models do not significantly differentiate between the two. However, voluntary surrender can save you from repossession fees and may make the lender more willing to negotiate on the deficiency balance.

How long can a repo stay on your credit if the dates are wrong?

If a creditor reports an incorrect date of first delinquency, the repo could appear to stay on your credit report longer than the legally allowed seven years. This is called “re-aging” and it is illegal. If you discover incorrect dates, file a dispute with the credit bureaus immediately. Under the FCRA, the bureaus must correct or remove inaccurate information within 30 days of your dispute.

What is a deficiency balance after repossession?

When your car is repossessed, the lender sells it (usually at auction) to recover some of the loan balance. If the sale price is less than what you owe, the remaining amount is called a deficiency balance. For example, if you owed $15,000 on your auto loan and the car sold at auction for $9,000, your deficiency balance would be $6,000. You are still legally responsible for paying this amount, and it may be sent to collections if unpaid.

Can I get a car loan after a repossession?

Yes, you can get a new auto loan after a repossession, though you will likely face higher interest rates and may need a larger down payment. Some lenders specialize in financing for borrowers with negative credit history. Focus on rebuilding your credit score first, as even a modest improvement can significantly reduce the interest rate you qualify for.

Take Control of Your Credit After a Repossession

A repossession is a serious setback, but it does not have to define your financial future. The seven-year clock is already ticking, and every step you take today to address the repo on your credit report accelerates your recovery.

Start by reviewing your credit report for errors. Many repo entries contain inaccuracies that can be disputed for earlier removal. Then focus on rebuilding positive credit history through on-time payments, low utilization, and strategic use of credit-building tools.

M1 Credit Solutions was built specifically for situations like this. Our AI-powered platform connects to your credit reports, identifies every negative item including repossession entries, and generates the dispute letters you need to fight back, all from one dashboard.

Start your free credit analysis with M1 Credit Solutions and take the first step toward credit recovery today.