Your credit score controls more of your life than you probably realize. It determines whether you get approved for a mortgage, what interest rate you pay on a car loan, and even whether a landlord rents to you. A low score can cost you tens of thousands of dollars over your lifetime, while a strong one opens doors to better financial opportunities at every turn.

The good news? You can fix your credit score yourself, without paying thousands to a credit repair company. Whether you are dealing with late payments, collections, errors on your report, or simply a thin credit file, this guide walks you through every step of the process. By the end, you will have a clear, actionable plan to raise your score and keep it there.

Here is what you need to know about how to fix your credit score:

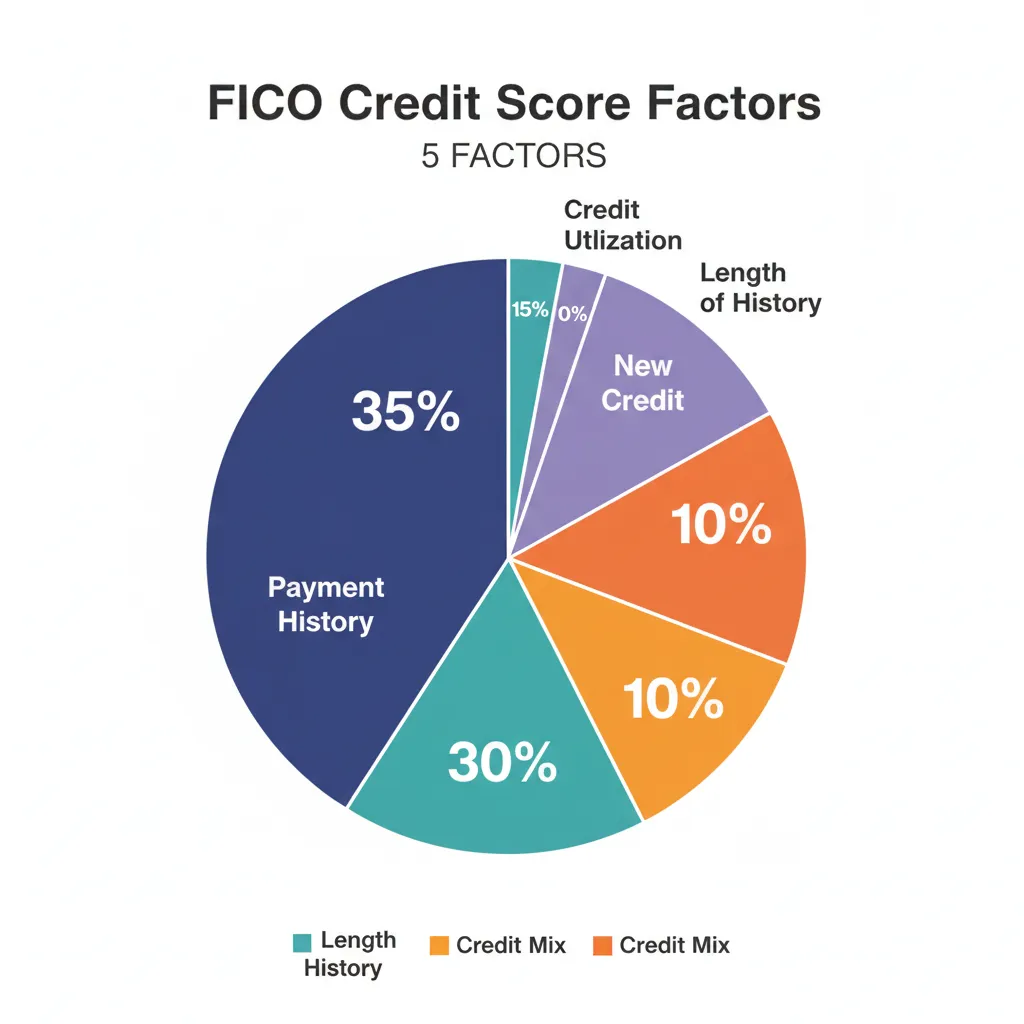

- Your credit score is built from five factors: payment history (35%), credit utilization (30%), length of history (15%), credit mix (10%), and new credit (10%).

- The fastest wins come from disputing credit report errors (30-45 day results) and paying down high credit card balances (one billing cycle).

- Building lasting credit improvement requires consistent on-time payments over three to six months, combined with smart use of tools like secured credit cards and credit-builder loans.

- You can do everything a credit repair company does yourself, for free, using your rights under the Fair Credit Reporting Act.

- AI-powered platforms like M1 Credit Solutions can automate the most time-consuming parts of the process, including report analysis and dispute letter generation.

What Is a Credit Score and Why Does It Matter?

A credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. Lenders, landlords, insurance companies, and even some employers use this number to evaluate how likely you are to repay borrowed money.

The two most common scoring models are FICO (used by 90% of top lenders) and VantageScore. While the exact formulas differ slightly, both evaluate the same core financial behaviors. Here is how credit score ranges generally break down:

- Excellent (800-850): Best rates and terms available

- Very Good (740-799): Qualifies for most premium offers

- Good (670-739): Considered acceptable by most lenders

- Fair (580-669): Subprime rates, limited options

- Poor (300-579): Difficulty getting approved for most credit

Why a few points matter more than you think: The difference between a 680 and a 720 credit score on a $300,000 30-year mortgage could mean paying $40,000+ more in interest over the life of the loan. Even small improvements can translate to significant savings.

The 5 Factors That Determine Your Credit Score

Understanding what drives your score is the first step to fixing it. Your FICO score is calculated from five weighted categories:

Payment History (35%)

This is the single most important factor. Lenders want to know: do you pay your bills on time? A single payment that is 30+ days late can drop your score by 60 to 100 points, and late payments stay on your report for seven years. The more recent the late payment, the more damage it causes.

Credit Utilization (30%)

Credit utilization measures how much of your available revolving credit you are using. If you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. Financial experts recommend keeping this below 30%, and people with the highest scores typically keep it under 10%.

Length of Credit History (15%)

This factor considers the age of your oldest account, the age of your newest account, and the average age of all accounts. A longer credit history signals stability. This is why closing old credit card accounts can actually hurt your score.

Credit Mix (10%)

Lenders like to see that you can manage different types of credit. A healthy mix might include revolving credit (credit cards) and installment loans (auto loans, mortgages, student loans, or personal loans).

New Credit Inquiries (10%)

Every time you apply for credit, a hard inquiry appears on your report and can temporarily lower your score by a few points. Multiple applications in a short period can signal financial distress to lenders.

Step 1: Get Your Credit Reports from All Three Bureaus

Before you can fix anything, you need to know exactly what you are working with. Your credit score is calculated from the information in your credit reports, and you have three of them, one from each major bureau:

- Equifax

- Experian

- TransUnion

How to get your free reports: Visit AnnualCreditReport.com, the only federally authorized source for free credit reports. You are entitled to one free report from each bureau every week, a program the FTC has confirmed is now permanent.

Why you need all three: Each bureau collects information independently. A creditor might report to one bureau but not another, which means errors or negative items could appear on one report but not the others. Always check all three.

What to look for as you review:

- Your personal information (name, address, Social Security number, employer)

- All open and closed accounts

- Payment history on each account

- Account balances and credit limits

- Public records (bankruptcies, liens, judgments)

- Hard inquiries from credit applications

Step 2: Identify and Dispute Errors on Your Credit Report

Credit report errors are more common than most people realize. According to a Federal Trade Commission (FTC) study, roughly one in five consumers had an error on at least one of their credit reports. These errors can unfairly drag your score down, and disputing them is one of the fastest ways to see improvement.

Common Errors to Watch For

- Accounts that do not belong to you (possible identity theft or mixed files)

- Incorrect payment statuses (payments marked late when they were on time)

- Duplicate accounts (the same debt listed more than once)

- Wrong balances or credit limits (inflating your utilization ratio)

- Outdated negative information (items that should have fallen off after 7 years)

- Incorrect personal information (wrong name, address, or Social Security number)

- Unauthorized hard inquiries (credit checks you did not authorize)

How to File a Dispute

- Document the error. Gather supporting evidence such as bank statements, payment receipts, or account correspondence.

- File with the credit bureau. You can dispute online through each bureau’s website (Equifax, Experian, TransUnion), by mail, or by phone. Filing by mail with certified delivery gives you a paper trail.

- Notify the furnisher. Also send a dispute to the company that reported the incorrect information (the “data furnisher”).

- Include supporting documents. Always send copies, never originals. Clearly explain what the error is and why it should be corrected.

- Wait for the investigation. By law, the bureau must investigate within 30 to 45 days and notify you of the results.

What to Do If Your Dispute Is Denied

If the bureau sides with the furnisher, you can:

- Submit a new dispute with additional evidence

- Add a 100-word consumer statement to your credit file explaining your side

- File a complaint with the Consumer Financial Protection Bureau (CFPB)

- Consult with a consumer rights attorney if the error involves significant financial harm

Pro tip: M1 Credit Solutions’ AI-powered platform can analyze your credit reports from all three bureaus, flag potential errors automatically, and generate customized dispute letters, saving you hours of manual work.

Step 3: Address Late Payments and Negative Items

Once you have disputed errors, it is time to tackle legitimate negative items on your report. While you cannot remove accurate information before its natural expiration, you can take steps to minimize the damage and begin rebuilding.

Bring Past-Due Accounts Current

If you have accounts that are currently past due, bringing them current should be your top priority. A past-due account continues to generate negative marks every month. Paying the past-due amount stops the bleeding and changes the account status to “current,” which looks significantly better to lenders.

Negotiate with Creditors

Many creditors are willing to work with you, especially if you have a history of on-time payments:

- Goodwill adjustment: Write a goodwill letter to your creditor asking them to remove a late payment from your record. This works best if you have an otherwise strong payment history.

- Pay-for-delete agreement: For collection accounts, you can sometimes negotiate a pay-for-delete arrangement where the collector agrees to remove the item from your report in exchange for payment.

- Hardship programs: Many creditors offer payment plans or forbearance programs if you are experiencing financial hardship.

Understand How Long Negative Items Stay

| Negative Item | Time on Report |

|---|---|

| Late payments (30, 60, 90+ days) | 7 years from the date of the missed payment |

| Collection accounts | 7 years from the original delinquency date |

| Chapter 7 bankruptcy | 10 years from the filing date |

| Chapter 13 bankruptcy | 7 years from the filing date |

| Hard inquiries | 2 years |

| Tax liens (unpaid) | Indefinitely (paid liens removed after 7 years) |

The impact of negative items decreases over time. A late payment from four years ago hurts far less than one from four months ago.

Step 4: Lower Your Credit Utilization

Reducing your credit utilization is one of the fastest ways to improve your credit score because utilization is recalculated every time your card issuer reports your balance to the bureaus, typically once per billing cycle.

Strategies to Lower Utilization Quickly

Pay down balances aggressively. Focus on cards that are closest to their limits first, since per-card utilization also matters.

Make multiple payments per month. Most card issuers report your balance on your statement closing date, not your payment due date. By making a payment before the statement closes, you can lower the balance that gets reported.

Request a credit limit increase. If your spending stays the same but your limit goes up, your utilization percentage drops automatically. Call your card issuer or request an increase through your online account. Many issuers will do a soft pull that does not affect your score.

Keep cards open even if unused. Closing a credit card reduces your total available credit, which increases your utilization ratio. An unused card with a $5,000 limit is actually helping your score.

Spread spending across multiple cards. Instead of maxing out one card, distribute charges across several to keep per-card utilization low.

The 30% Rule (and Why 10% Is Better)

While the commonly cited threshold is 30%, data from FICO shows that consumers with the highest credit scores (800+) typically maintain utilization under 10%. Aim for below 30% as a minimum, and work toward single-digit utilization for the best results.

Step 5: Build Positive Payment History Going Forward

Since payment history is 35% of your score, establishing a consistent record of on-time payments is the most powerful long-term strategy for credit improvement.

Set Up Automatic Payments

Enroll in autopay for at least the minimum payment on every account. This creates a safety net that prevents you from ever being marked as late. You can always pay more than the minimum before the due date.

Use Calendar Reminders

Set reminders one week and two days before each bill is due. This gives you time to verify funds are available and schedule the payment.

Prioritize Bills That Report to Credit Bureaus

Not all bills appear on your credit report. Focus first on accounts that are reported: credit cards, loans, mortgage payments, and any accounts with credit reporting. Utility and rent payments typically are not reported unless you use a third-party reporting service.

Address Missed Payments Immediately

If you miss a payment, pay it as soon as possible. Payments are typically not reported as late until they are 30+ days past due. If you pay within that window, it may not appear on your report at all.

Step 6: Build Credit with the Right Tools

If you have a thin credit file or are rebuilding after significant damage, you need to add positive tradelines to your report. Here are the most effective tools:

Secured Credit Cards

A secured credit card (or one of the best credit cards for rebuilding credit with no annual fee) typically requires a refundable security deposit that typically becomes your credit limit. Use it for small purchases and pay the balance in full every month. The issuer reports your on-time payments to the credit bureaus, building positive history.

Credit-Builder Loans

A credit-builder loan places the loan amount into a locked savings account while you make monthly payments. Each payment is reported to the bureaus. When you finish paying, you receive the funds. It is a savings plan and credit builder in one.

Become an Authorized User

Ask a trusted family member or partner with excellent credit to add you as an authorized user on one of their credit cards. Their positive payment history and low utilization can appear on your credit report, giving your score a lift. You do not even need to use the card.

Experian Boost and Alternative Data

Services like Experian Boost let you add on-time utility, phone, and streaming service payments to your Experian credit report. This can provide an immediate score increase by giving you credit for bills you are already paying.

Report Rent Payments

Rent is typically the largest monthly expense for many people, yet it usually goes unreported to credit bureaus. Third-party rent-reporting services can add these on-time payments to your credit file, creating another positive tradeline.

Step 7: Manage New Credit Applications Strategically

Every credit application triggers a hard inquiry that can temporarily lower your score. While one inquiry typically causes a drop of less than 5 points, multiple inquiries in a short period can add up.

Best Practices for New Credit

- Only apply when you need it. Avoid opening accounts just for a sign-up bonus if you are focused on rebuilding.

- Check for prequalification first. Many lenders offer prequalification with a soft pull that does not affect your score.

- Rate-shop within a focused window. If you are shopping for a mortgage, auto loan, or student loan, multiple inquiries within a 14 to 45 day window (depending on the scoring model) count as a single inquiry.

- Space out credit card applications. Wait at least 3 to 6 months between credit card applications to minimize the impact on your score.

What to Expect: Your Credit Score Repair Timeline

Fixing your credit is not an overnight process, but you can see meaningful progress faster than you might expect. Here is a realistic timeline:

Quick Wins (1-3 Months)

- Dispute errors: Bureaus must respond within 30 to 45 days. Removing even one error can boost your score by 20 to 100+ points.

- Pay down high balances: Utilization changes are reflected in your score within one to two billing cycles.

- Become an authorized user: Positive history can appear on your report within 30 to 60 days.

Steady Progress (3-6 Months)

- Build a payment history streak: Three to six consecutive months of on-time payments begins to establish a positive pattern.

- Secured card usage: Regular use and on-time payment of a secured card starts building a meaningful track record.

Significant Improvement (6-12 Months)

- Consistent on-time payments: Six to twelve months of perfect payment history can produce a noticeable score increase.

- Reduced debt impact: As you pay down balances, both your utilization and overall debt levels improve.

Long-Term Growth (1-2+ Years)

- Aging of negative items: Late payments and collections lose impact over time.

- Credit history length: As your accounts age, this factor strengthens.

- Full recovery from major events: Bankruptcy recovery typically takes 2 to 4 years of responsible credit management.

How to Maintain a Good Credit Score for Life

Fixing your credit score is just the beginning. Maintaining it requires consistent habits:

- Pay every bill on time, every time. Set up autopay as a safety net.

- Keep credit utilization below 30%. Aim for under 10% for the best scores.

- Monitor your credit reports regularly. Check all three reports at least quarterly through AnnualCreditReport.com.

- Keep old accounts open and active. Use old cards for a small recurring charge and autopay the balance.

- Limit new credit applications. Only apply when you genuinely need new credit.

- Review your reports for errors annually. Errors can appear at any time, so ongoing vigilance is important.

- Use credit monitoring tools. AI-powered platforms can alert you to changes and help you stay proactive.

Frequently Asked Questions

How long does it take to fix a credit score?

The timeline depends on your starting point and the issues affecting your score. Error disputes can produce results in 30 to 45 days. Paying down high balances can improve your score within one to two billing cycles. Building a strong payment history takes three to six months of consistent on-time payments. Major events like bankruptcy require one to two years of responsible credit management before significant recovery.

Can I fix my credit score myself without paying a company?

Yes. Everything a credit repair company can do legally, you can do yourself. The FTC confirms this. You can pull your free credit reports, identify errors, write and send dispute letters, negotiate with creditors, and build positive credit habits on your own. Tools like M1 Credit Solutions’ AI-powered platform can streamline the process by automatically analyzing your reports and generating dispute letters, making DIY credit repair faster and more effective.

What is the fastest way to raise my credit score?

The quickest strategies are: (1) Dispute and remove errors from your credit reports, which can produce results in 30 to 45 days. (2) Pay down credit card balances below 30% utilization, which is reflected in your score within one billing cycle. (3) Become an authorized user on a positive account. (4) Use Experian Boost to add utility and streaming payments to your report.

Does checking my own credit score hurt it?

No. When you check your own credit, it is recorded as a “soft inquiry” and has zero impact on your score. Only “hard inquiries” from lender credit applications affect your score. You can check your credit as often as you like without any negative consequences.

Should I close old credit cards I no longer use?

Generally, no. Closing old accounts can hurt your score in two ways: it reduces your total available credit (increasing your utilization ratio) and can shorten the average age of your credit history. Instead, keep old cards active by making a small purchase every few months and paying it off immediately. If the card has an annual fee, call the issuer and ask to downgrade to a no-fee version.

Is it better to pay off a collection or leave it alone?

In most cases, paying off a collection is the better move. While the collection record remains on your report, a “paid” status looks better to lenders than an outstanding debt. With newer FICO scoring models (FICO 9 and 10), paid collections have zero impact on your score. You can also try to negotiate a pay-for-delete agreement before making payment.

How much can my credit score increase in 30 days?

It depends on your situation. If you have errors removed or pay down high balances, you could see a 20 to 100+ point improvement within 30 days. Someone with maxed-out credit cards who pays them down to 10% utilization could see one of the most dramatic short-term improvements.

What credit score do I need to buy a house?

Minimum requirements vary by loan type: FHA loans require a minimum score of 580 (or 500 with a 10% down payment), conventional loans typically require 620+, and VA loans have no official minimum but most lenders want 620+. However, a score of 740 or higher will qualify you for the best mortgage rates and terms.

Written by Tayde Aburto, founder of M1 Credit Solutions and financial educator with over a decade of experience helping individuals and small business owners take control of their financial futures. For more details, see our guide on build business credit.