A bad credit score costs you real money every single day. It means higher interest rates on loans, bigger deposits on apartments, and rejection letters from credit card companies. The credit repair industry knows this, and they charge hundreds or even thousands of dollars to do work that you have every legal right to do yourself.

If you were denied an apartment because of credit, start by reviewing the screening decision and checking the reports used before you plan your next application.

Ready to fix your credit the smart way? M1 Credit Solutions uses AI to analyze your reports, find errors, and generate custom dispute letters (including those for removing a repo from your credit) in minutes.

DIY credit repair is the process of identifying errors, outdated items, and inaccurate negative marks on your credit reports and disputing them directly with the credit bureaus. It is your right under federal law, and with the right tools and knowledge, you can do it just as effectively as any agency.

This guide covers the entire process from start to finish. You will learn how to pull your credit reports, identify what is actually hurting your score, write effective dispute letters, and monitor your progress. We will also look at how AI-powered platforms like M1 Credit Solutions have transformed DIY credit repair from a tedious paper-based process into something you can manage from your phone. M1 also offers an AI-powered DIY credit repair platform for people who want help generating dispute letters while staying in control of the process.

- You have the legal right to repair your credit yourself. The Fair Credit Reporting Act (FCRA) requires credit bureaus to investigate any item you dispute and remove anything they cannot verify within 30 days.

- Start by getting all three credit reports. Errors and inaccuracies are common. Pulling reports from Experian, Equifax, and TransUnion gives you the full picture of what is dragging your score down.

- Dispute strategically, not randomly. Focus on items with the highest negative impact first: late payments, collections, charge-offs, and accounts that are not yours.

- AI tools have changed the game. Platforms like M1 Credit Solutions can analyze your reports automatically, identify the most damaging items, and generate custom dispute letters in minutes instead of hours.

- Patience and consistency win. Most people see meaningful score improvements within 3 to 6 months of starting the dispute process.

What Is DIY Credit Repair?

DIY credit repair means taking direct action to improve your credit score without hiring a third-party credit repair company. Instead of paying someone else to manage the process, you handle it yourself by reviewing your credit reports, identifying errors or questionable items, and filing disputes with the credit bureaus.

One common question is whether paying off a collection account will raise your credit score. The answer depends on which scoring model is used. Read more: does paying off collections increase your credit score.

The term “repair” can be misleading. You are not fabricating a new credit history. You are exercising your rights under the Fair Credit Reporting Act to ensure that the information on your credit reports is accurate, complete, and verifiable. If something on your report is wrong, outdated, or unverifiable, the credit bureau is legally required to correct or remove it.

Here is what DIY credit repair can address:

- Inaccurate personal information (wrong name, address, or employer)

- Accounts that do not belong to you (identity theft or mixed files)

- Late payments reported incorrectly (you paid on time but it shows late)

- Duplicate accounts (the same debt listed more than once)

- Outdated negative items (items past the 7-year reporting window)

- Incorrect account balances or credit limits

- Collections for debts you do not owe

- Charge-offs that have been paid but still show as unpaid

What DIY credit repair cannot do is remove legitimate negative items that are accurately reported. If you genuinely missed a payment, that record is within the bureau’s rights to report. However, creditors and collection agencies make reporting errors far more often than most people realize, which is exactly why the dispute process exists.

Your Legal Rights Under the FCRA

The Fair Credit Reporting Act is the backbone of DIY credit repair. Understanding your rights under this law gives you real power in the process.

Key FCRA Protections

- Right to dispute. You can dispute any item on your credit report that you believe is inaccurate, incomplete, or unverifiable. The credit bureau must investigate your dispute, typically within 30 days.

- Burden of proof is on the bureau. When you file a dispute, the credit bureau must contact the creditor who reported the item and verify it. If the creditor cannot verify the item, the bureau must remove it from your report.

- Right to free annual reports. You are entitled to one free credit report per year from each of the three major bureaus through AnnualCreditReport.com.

- Right to know who accessed your report. You can see every company that has pulled your credit, which helps you identify unauthorized inquiries.

- Right to add a consumer statement. If a dispute does not result in removal, you can add a 100-word statement to your report explaining the circumstances.

- Right to sue. If a credit bureau violates the FCRA by failing to investigate or correct inaccurate information, you have the right to take legal action.

These protections are why DIY credit repair works. The law is on your side, and credit bureaus are legally obligated to respond to your disputes.

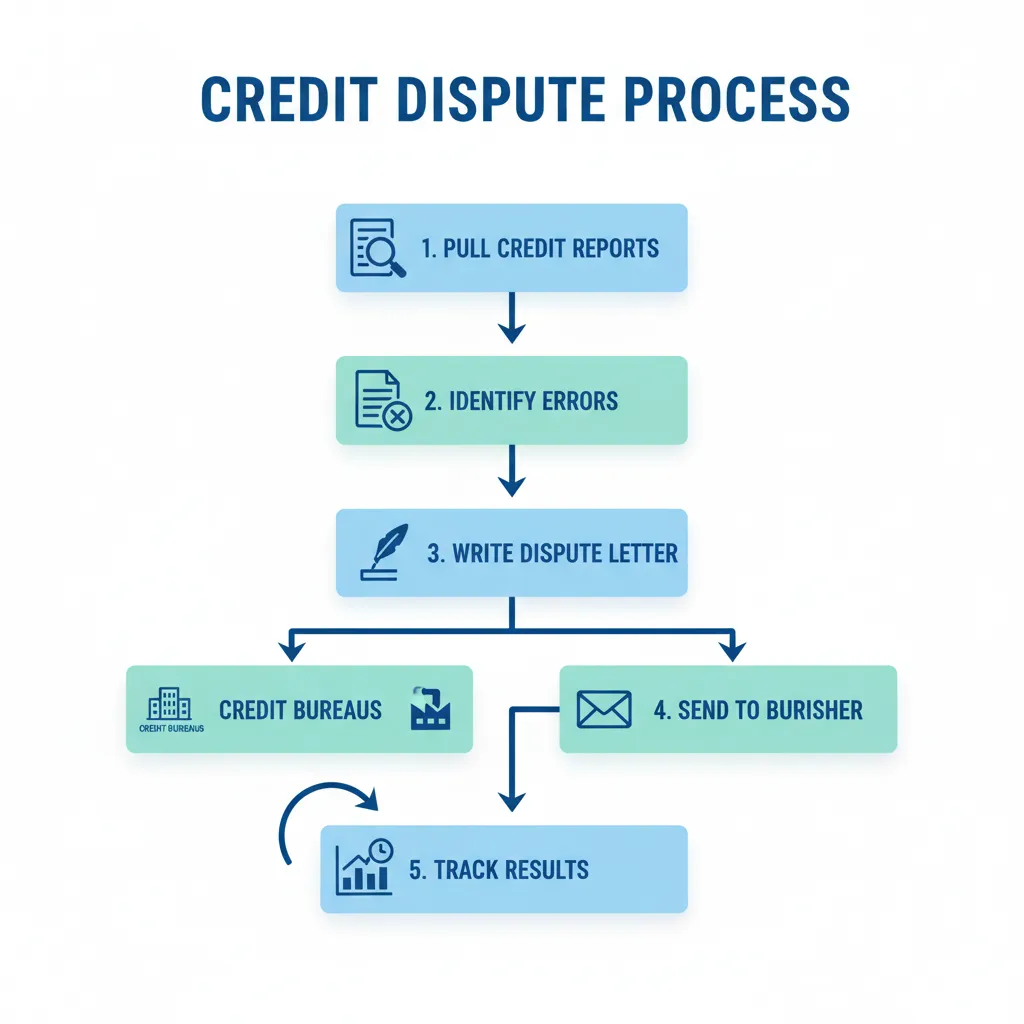

Step 1: Pull Your Credit Reports from All Three Bureaus

Before you can fix anything, check your credit report for free to see exactly what is on your reports. Each of the three major credit bureaus (Experian, Equifax, and TransUnion) maintains its own file on you, and they often contain different information.

How to get your reports:

- Visit AnnualCreditReport.com to request your free reports

- You can also request reports directly from each bureau’s website

- If you have been denied credit within the last 60 days, you are entitled to an additional free copy from the bureau that provided the report

Important: Do not confuse credit reports with credit scores. Your report is the detailed history of your credit activity. Your score is a number calculated from that history. You need the full report to identify what needs to be disputed.

Pull all three reports because errors may appear on one but not the others. A collection account might show on your Equifax report but not on your Experian report, for example. You need the complete picture.

Step 2: Analyze Your Reports and Identify Errors

This is where most people get overwhelmed. Credit reports are dense documents filled with codes, abbreviations, and account details that can be hard to interpret. But this step is critical because it determines what you will dispute.

What to look for:

Personal Information Errors

- Misspelled name or wrong name entirely

- Incorrect Social Security Number

- Wrong address (current or previous)

- Incorrect employer information

Account Errors

- Accounts you did not open (possible identity theft)

- Incorrect payment statuses (showing late when you paid on time)

- Wrong balance amounts or credit limits

- Duplicate listings of the same account

- Accounts showing as open when you closed them

Negative Item Review

- Late payments older than 7 years that should have fallen off

- Collections for debts that are not yours

- Charge-offs that have been settled but still show a balance

- Bankruptcies older than 10 years still on your report

- Tax liens or judgments with incorrect details

Go through each report line by line. Highlight or make a list of every item you plan to dispute. The more specific you are about what is wrong and why, the stronger your dispute will be.

This is where technology can save you significant time. M1 Credit Solutions AI software connects to your credit reports from all three bureaus and uses AI to automatically identify negative items, errors, and inaccuracies. Instead of spending hours reading through pages of credit data, the platform highlights exactly what is hurting your score and what you should dispute first.

Step 3: Write and Send Your Dispute Letters

Once you have identified the items you want to dispute, you need to formally notify the credit bureaus. This is done through dispute letters sent to each bureau that is reporting the inaccurate information.

What to Include in a Dispute Letter

Every dispute letter should contain:

- Your full name, address, and date of birth

- Your Social Security Number (for identification)

- The specific item you are disputing (account name, account number, and the reason it is inaccurate)

- Your request (investigation, correction, or removal)

- Supporting documentation (copies of payment receipts, correspondence with creditors, identity theft reports, or anything that supports your claim)

How to Send Disputes

- By mail (recommended for documentation). Send dispute letters via certified mail with return receipt requested. This creates a paper trail proving the bureau received your dispute.

- Online. Each bureau has an online dispute portal. This is faster but gives you less control over your documentation.

- By phone. Not recommended because there is no written record of what you disputed.

Where to Send Disputes

- Equifax: P.O. Box 740256, Atlanta, GA 30374

- Experian: P.O. Box 4500, Allen, TX 75013

- TransUnion: P.O. Box 2000, Chester, PA 19016

After the bureau receives your dispute, they have 30 days (45 days if you provide additional information during the investigation) to investigate and respond.

Need help drafting your dispute letters? Check out our pay-for-delete letter guide for step-by-step templates and strategies that have helped others remove collection accounts from their credit reports.

The AI Advantage for Dispute Letters

Writing effective dispute letters takes time and requires knowing the right language and legal references. This is one of the biggest advantages of using an AI-powered platform like M1 Credit Solutions. M1’s AI analyzes your specific credit situation and generates customized dispute letters designed for maximum effectiveness. Instead of using generic templates that bureaus can easily dismiss, you get letters tailored to the specific issues on your report, the specific bureaus involved, and the specific legal provisions that apply to your case.

Step 4: Track Bureau Responses and Follow Up

Filing a dispute is not a one-and-done action. You need to track responses, follow up on incomplete investigations, and sometimes escalate.

What happens after you dispute:

- The bureau contacts the creditor who reported the item (called a “furnisher”)

- The furnisher has a limited time to verify the information

- The bureau sends you the results of the investigation

- If the item is verified as accurate, it stays. If it cannot be verified, it must be removed.

Common outcomes:

- Deleted. The item is removed from your report. This is the best outcome and directly improves your score.

- Updated. The information is corrected (for example, a late payment status is changed to on-time). This also helps your score.

- Verified. The furnisher verified the information and it stays on your report. You can re-dispute with additional evidence, file a complaint with the CFPB, or add a consumer statement.

If items are verified but you believe they are still inaccurate:

- Send a follow-up dispute with additional documentation

- File a complaint with the Consumer Financial Protection Bureau (CFPB)

- Dispute directly with the furnisher (the creditor or collection agency)

- Consult a consumer rights attorney if the violation is clear

Keep detailed records of every letter you send, every response you receive, and every change to your reports.

Step 5: Build Positive Credit While Disputing

While you work on removing negative items, you should simultaneously build new positive credit history. Removing negatives and adding positives is the fastest path to a higher score.

- Make every payment on time. Payment history is the single largest factor in your credit score (35% of your FICO score).

- Keep credit utilization below 30%. If you have a credit card with a $1,000 limit, keep your balance below $300.

- Get a secured credit card. If you have limited credit or very low scores, a secured card lets you build positive history with a cash deposit as collateral.

- Become an authorized user. If a family member has a credit card with a long, positive payment history, being added as an authorized user can boost your score.

- Keep old accounts open. The age of your credit history matters.

For a deeper dive into these strategies, our guide on how to improve your credit score covers each factor in detail.

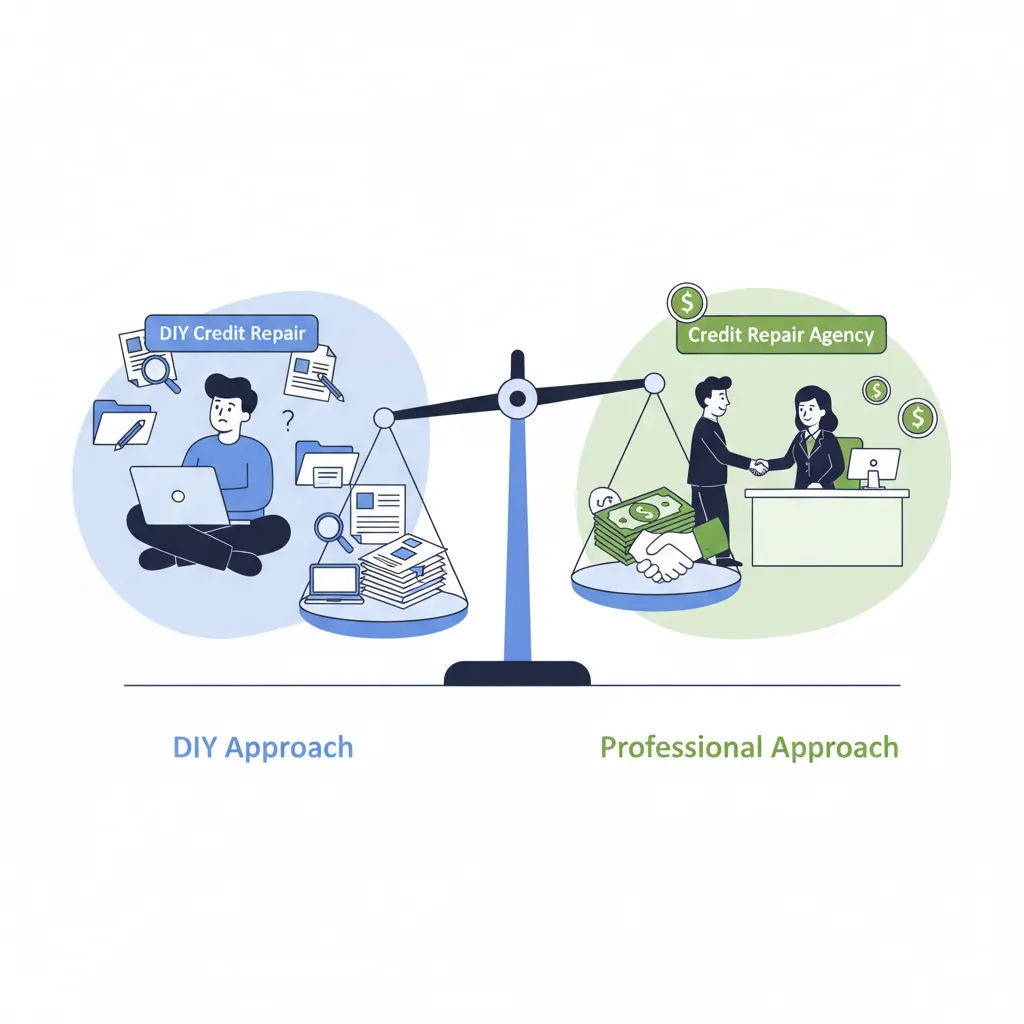

DIY Credit Repair vs. Hiring a Credit Repair Company

One of the biggest questions people face is whether to handle credit repair themselves or pay a company to do it. Here is an honest comparison:

| Factor | DIY Credit Repair | Professional Credit Repair |

|---|---|---|

| Cost | Free (or low-cost with tools) | $50-$150/month, often for 6-12 months |

| Control | Full control over every dispute | Company handles disputes on your behalf |

| Speed | Depends on your consistency | Not necessarily faster; same bureau timelines |

| Effectiveness | Equally effective if done correctly | Companies use the same dispute process |

The key insight is that credit repair companies use the exact same dispute process available to you. The FCRA does not give them any special powers. Where professional companies add value is experience with complex cases, but this expertise is increasingly available through AI-powered platforms.

How AI Has Transformed DIY Credit Repair

Traditional DIY credit repair meant printing out your credit reports, reading through them with a highlighter, writing dispute letters from generic templates, and mailing them. AI-powered platforms have fundamentally changed this:

Automated Report Analysis

AI connects to your reports from all three bureaus and instantly identifies every negative item, error, and inaccuracy, prioritized by impact on your score.

Custom Dispute Letter Generation

AI generates unique, customized dispute letters that reference specific issues, cite relevant legal provisions, and use language designed to produce results.

Progress Tracking

Real-time dashboards show dispute status, score changes, and overall progress.

Strategy Optimization

AI analyzes dispute outcome patterns and recommends the most effective approach for each type of negative item.

M1 Credit Solutions was built to bring these capabilities to everyday consumers. The platform runs an AI-powered analysis, generates customized dispute letters, and tracks progress through a real-time dashboard. It is the modern evolution of DIY credit repair.

Get Started with M1 Credit Solutions →

DIY Credit Repair: Manual vs. AI-Powered — What’s the Difference?

Understanding the difference between traditional manual DIY credit repair and modern AI-powered DIY credit repair is essential for choosing the right approach. Both are legal, both respect your rights under the FCRA, and both put you in control of the process. The key difference is the time, effort, and consistency required.

Manual DIY credit repair means pulling your reports from each bureau individually, reading through pages of data by hand, writing dispute letters from generic templates, printing and mailing them via certified mail, and tracking responses in a spreadsheet. It works, but it demands significant time and attention to detail. Each cycle takes 30 to 45 days, and a single mistake in your dispute letter can cost you a month.

AI-powered DIY credit repair uses machine learning to automate the heavy lifting. Platforms like M1 Credit Solutions connect directly to your credit reports, analyze every item using advanced algorithms, and generate customized dispute letters tailored to each specific issue on your report. Instead of spending hours reading credit data, you get a prioritized list of what to dispute and letters ready to send.

| Factor | Manual DIY | AI-Powered DIY (M1 Credit Solutions) |

|---|---|---|

| Report Analysis | Read manually, 1-2 hours per bureau | Automated scan in seconds |

| Dispute Letters | Generic templates, customizing is tedious | AI generates unique letters for each item |

| Speed | 3-6 months to see results | Often faster due to optimized strategy |

| Tracking | Spreadsheet you maintain | Real-time dashboard updates |

| Monthly Cost | Minimal (postage, printing) or free | Starting at $29.99/month |

| Success Rate | Depends on your knowledge and consistency | AI optimizes each dispute for best results |

The bottom line: manual DIY credit repair is like fixing a car with a wrench set. AI-powered DIY is like fixing the same car with a diagnostic computer and a power drill. Both get the job done, but one is dramatically faster and more efficient. M1 Credit Solutions gives you the AI-powered approach while keeping you in full control of your credit repair journey.

Common DIY Credit Repair Mistakes to Avoid

1. Disputing Everything at Once

Sending dozens of disputes simultaneously can trigger bureaus to classify your disputes as “frivolous.” Start with 3 to 5 items per bureau per round.

2. Not Keeping Records

Always use certified mail or keep screenshots of online disputes. Save every response.

3. Ignoring the Furnisher

You can dispute directly with the company that reported the information. Furnisher disputes can be more effective.

4. Using Only Generic Templates

Personalize your disputes with specific details about why the information is inaccurate.

5. Giving Up Too Soon

Most people see significant results within 3 to 6 months. Stay consistent.

6. Not Building Positive Credit Simultaneously

Removing negatives is only half the equation. Build positive credit through on-time payments and responsible use.

7. Not Leveraging Technology

Doing everything manually saves money on software, but it costs you time. AI-powered platforms like M1 Credit Solutions can analyze reports and generate dispute letters in minutes instead of hours. The time you save can be redirected to monitoring results and planning your next moves. Given that pay-for-delete letters and debt validation strategies require careful follow-up, the efficiency of technology makes a real difference over a multi-month repair timeline.

How Long Does DIY Credit Repair Take?

- Week 1-2: Pull reports, analyze them, identify disputes

- Week 3-4: Send first round of dispute letters

- Month 2-3: Receive results, send follow-up disputes

- Month 3-6: Continue the cycle, build positive credit

- Month 6-12: Most items addressed, positive habits reflected in score

Some people see 50 to 100 point improvements within 3 to 6 months. The key is consistency.

Frequently Asked Questions

Is DIY credit repair legal?

Absolutely. The FCRA explicitly gives every consumer the right to dispute inaccurate information. Credit bureaus are legally required to investigate and correct or remove anything they cannot verify.

How much does DIY credit repair cost?

It can be completely free. AI-powered platforms like M1 Credit Solutions offer a more efficient approach at a fraction of what traditional credit repair companies charge.

Can DIY credit repair hurt my credit score?

No. Filing a dispute does not negatively affect your score. Successful disputes improve it.

What is the difference between credit repair and credit counseling?

Credit repair removes inaccurate items from reports. Credit counseling helps manage debts and budgets. For details, read our guide on credit repair vs. credit counseling.

Should I use credit repair software or do it manually?

Software and AI tools dramatically speed up the process. The best credit repair software combines AI analysis with an easy-to-use interface.

Can I repair my credit score if I have collections?

Yes. Collections are commonly disputed and removed. Our self-credit repair guide covers strategies for dealing with collections.

Start Repairing Your Credit Today

Every day you wait is a day you are paying more in interest. If homeownership is your goal, learn how to get mortgage-ready. Start by reviewing your credit reports and identifying what needs to be fixed. M1 Credit Solutions gives you AI-powered report analysis, customized dispute letters, and a real-time dashboard to track your progress. Business owners should also explore building business credit as a separate financial asset.