Secured business credit cards can help founders qualify for revolving credit when business history is thin or personal credit is less than perfect. They are not the right fit for every company, but they can be a practical bridge between cash-only operations and stronger business financing options.

Ready to build stronger business credit?

M1 Credit Solutions helps you repair your personal credit and build a solid business credit profile, so you can qualify for better cards and financing.

What is a secured business credit card?

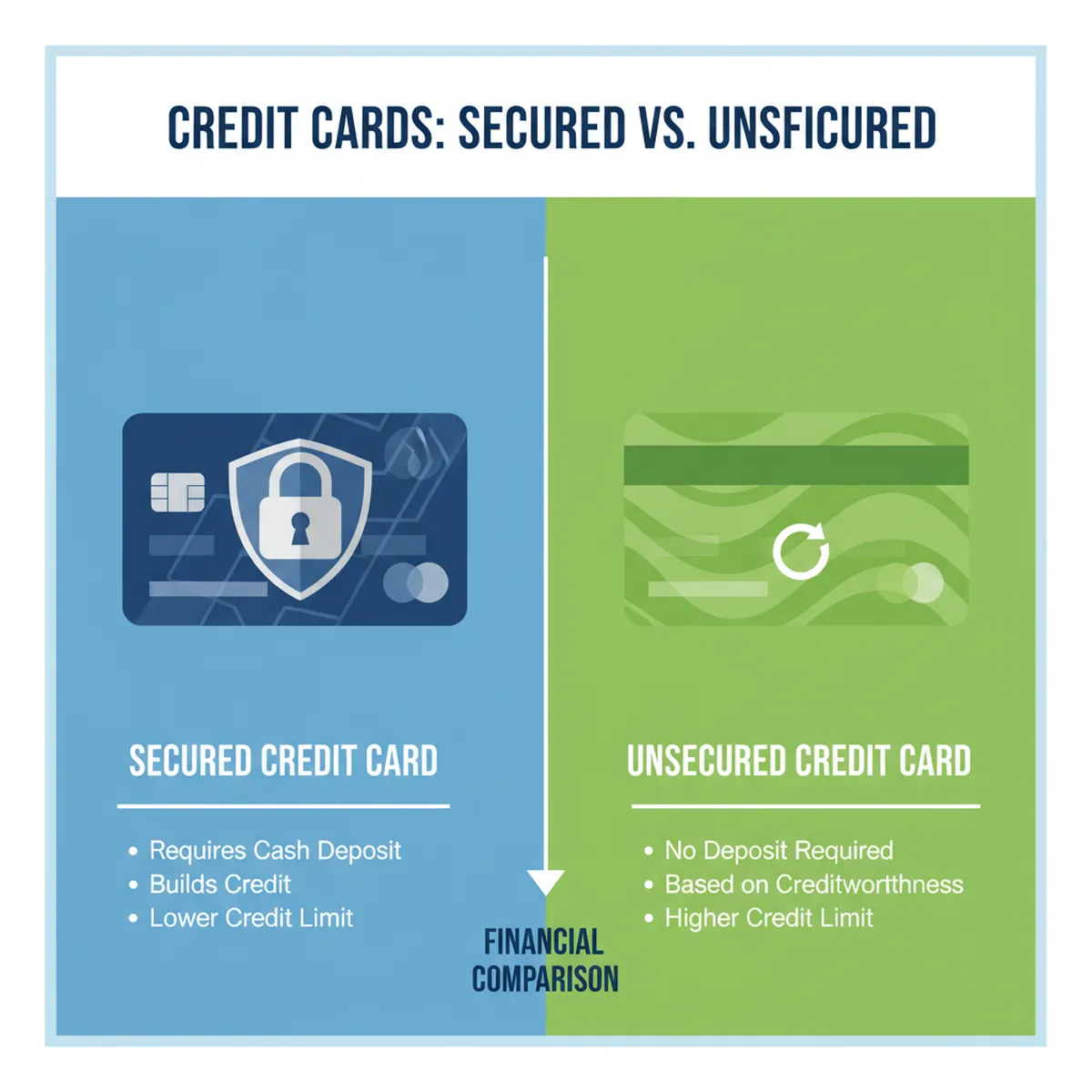

A secured business credit card requires a refundable security deposit. In most cases, that deposit sets all or part of your credit limit. If you put down $1,000, your usable limit may be $1,000 or slightly less depending on the issuer.

Unlike unsecured business credit cards, the bank has collateral backing the account. That lowers lender risk and gives newer businesses, startups, and owners with limited business credit a better chance of approval.

The most important question is not just whether you can get approved. It is whether the card reports to the right business credit bureaus, supports disciplined usage, and fits into a broader plan to build vendor credit, trade lines, and financing readiness.

How secured business credit cards work

- You apply with the issuer using business and personal information.

- If approved, you submit a security deposit.

- The issuer opens the card with a limit tied to the deposit.

- You use the card for routine business expenses and repay on time.

- Positive account history may help you qualify for unsecured products later.

That structure makes these cards different from merchant accounts, term loans, or lines of credit. They are best used for recurring spend you can pay off in full each month, such as fuel, software, subscriptions, internet service, shipping, and small inventory purchases.

Secured vs. unsecured business credit cards

| Factor | Secured business card | Unsecured business card |

|---|---|---|

| Deposit required | Yes | No |

| Approval standards | Usually easier | Usually stricter |

| Credit limits | Often lower at the start | Can be higher |

| Rewards/perks | Often limited | Usually stronger |

| Best use case | Credit building and early-stage access | Established businesses with stronger profiles |

If your company can already qualify for an unsecured card with better rewards, a secured option may be unnecessary. If approvals are limited, utilization is hard to manage, or your business file is still developing, a secured card may be the smarter short-term move.

Who should consider a secured business credit card?

- Startups without established business credit history

- LLCs and corporations that are early in the credit-building process

- Owners rebuilding after personal credit issues

- Businesses that want a controlled way to establish payment history

- Founders preparing for larger funding products later

A secured business credit card is usually not the end goal. It is a stepping stone. The right strategy is to use it alongside foundational business credit work, such as setting up your entity correctly, getting an EIN, opening a business bank account, listing consistent business information, and building trade references where relevant.

Qualification requirements to expect

Issuers do not all underwrite the same way, but these are the most common requirements:

- A valid business entity or sole proprietor information

- An EIN or Social Security number, depending on structure

- Verifiable contact and business details

- A security deposit from available cash

- A personal guarantee in many cases

Many founders assume a deposit means no credit review. That is not always true. Some issuers still review personal credit, business revenue, time in business, and recent delinquencies. The deposit reduces risk, but it does not automatically eliminate underwriting.

Top features to compare before choosing a card

- Business credit reporting: Confirm which bureaus receive payment data.

- Minimum and maximum deposit: Make sure the cash requirement fits your operating budget.

- Annual fee: Low-value cards can get expensive if fees pile up.

- APR: Important if you may ever carry a balance, though full payoff should be the plan.

- Graduation path: Some issuers allow movement to unsecured products after strong history.

- Employee cards and spend controls: Useful for growing teams.

- Online account management: Alerts, autopay, and easy expense tracking matter.

How to use a secured business card to build business credit

- Keep utilization low, ideally under 30 percent and often lower.

- Pay before the statement closes when spend spikes.

- Use the card every month for predictable business purchases.

- Set autopay to avoid missed payments.

- Review bureau reporting after a few cycles.

- Request graduation or apply for stronger products only after stable history is established.

Used correctly, a secured business card can help support the credibility of your business profile over time. Used poorly, it becomes an expensive tool that ties up cash, adds fees, and does little for financing readiness.

Common mistakes to avoid

- Choosing a card without confirming business bureau reporting

- Using most of the limit every month

- Carrying high-interest balances

- Opening the account without a larger credit-building plan

- Applying too early for multiple other credit products

- Mixing heavy personal spending with business expenses

What are the top options in 2026?

The market for true secured business credit cards is smaller than many founders expect. Some business owners end up comparing a mix of secured consumer cards used for startup cash flow, corporate charge cards for stronger businesses, and fintech products with alternative underwriting. Because offers change often, focus on the criteria above instead of chasing a single list that may age quickly.

As you compare current offers, prioritize reporting quality, deposit flexibility, fee structure, and whether the issuer provides a realistic graduation path. A modest card that actually helps you build business credit is more valuable than a flashy card that reports poorly or traps cash for too long.

When to skip secured cards and look at other funding options

If your company needs larger working capital, equipment financing, or a true revolving line of credit, a secured business credit card may be too small to matter. In that case, improving your credit profile and preparing lender-ready documentation may create a better path to real funding products.

That is especially true for owners who already have revenue, clean bank statements, and a defined financing use case. A small secured limit will not replace strategic funding. It only helps establish disciplined revolving credit behavior.

Final takeaway

Secured business credit cards make sense when access matters more than perks. They are most useful for businesses that need to start building history, prove payment discipline, and create a stronger foundation for future approvals. The key is choosing a card that reports properly and using it as part of a broader business credit strategy, not as a standalone fix.

Frequently asked questions

Do secured business credit cards build business credit?

They can, but only if the issuer reports your account activity to relevant business credit bureaus. Always verify reporting before you apply.

Do you need good personal credit to get a secured business credit card?

Not always, but many issuers still review personal credit and may require a personal guarantee. The deposit helps, but it does not remove all underwriting standards.

How much is the security deposit?

It depends on the issuer. Some cards start with a few hundred dollars, while others require larger deposits tied directly to the requested credit limit.

Can a secured business card help you qualify for better financing later?

It can support a stronger profile when combined with on-time payments, low utilization, clean business records, and broader business credit-building activity.