Your credit score is a three-digit number that can save you thousands of dollars or cost you just as much. Whether you are applying for a mortgage, financing a car, or opening a credit card, lenders use this number to decide if you qualify and what interest rate you will pay.

Check your credit score and start improving it today with M1 Credit Solutions

But what counts as a “good” credit score? The answer depends on which scoring model a lender uses and what financial product you are pursuing. In this guide, we break down every credit score range, explain how scores are calculated, and share actionable steps to raise yours starting today.

Key Takeaways

- A good credit score is 670 to 739 on the FICO scale, the model used in roughly 90% of U.S. lending decisions.

- Credit scores range from 300 to 850 for both FICO and VantageScore models.

- The average American credit score is approximately 715, placing most consumers in the “good” category.

- Five factors determine your score: payment history (35%), amounts owed (30%), credit history length (15%), new credit (10%), and credit mix (10%).

- Moving from a “fair” score to a “good” score can save you tens of thousands of dollars in interest over the life of a mortgage or auto loan.

- You can check your score for free and take steps to improve it without paying a credit repair agency.

Understanding Credit Scores: The Basics

A credit score summarizes your borrowing and repayment history into a single number. Lenders, landlords, insurance companies, and even some employers review this number to assess financial risk.

The two primary scoring models in the United States are:

- FICO Score – Created by the Fair Isaac Corporation, used by 90% of top lenders according to myFICO.

- VantageScore – Developed jointly by Experian, Equifax, and TransUnion. Commonly used by free credit monitoring apps and some lenders.

Both models use a 300 to 850 scale, but they weigh certain factors differently. When a lender “pulls your credit,” they are almost always looking at a version of your FICO score.

FICO Score vs. VantageScore: Key Differences

| Feature | FICO Score | VantageScore |

|---|---|---|

| Scale | 300–850 | 300–850 |

| Used by lenders | ~90% of top lenders | Growing adoption |

| Minimum history | 6 months, 1 active account | 1 month, 1 account |

| “Good” range | 670–739 | 661–780 |

| Latest version | FICO Score 10T | VantageScore 4.0 |

For most financial decisions, your FICO score is the one that matters most.

Credit Score Ranges: Where Do You Stand?

Understanding credit score ranges helps you gauge where you fall and what opportunities are available to you. Here is how both major scoring models categorize credit scores.

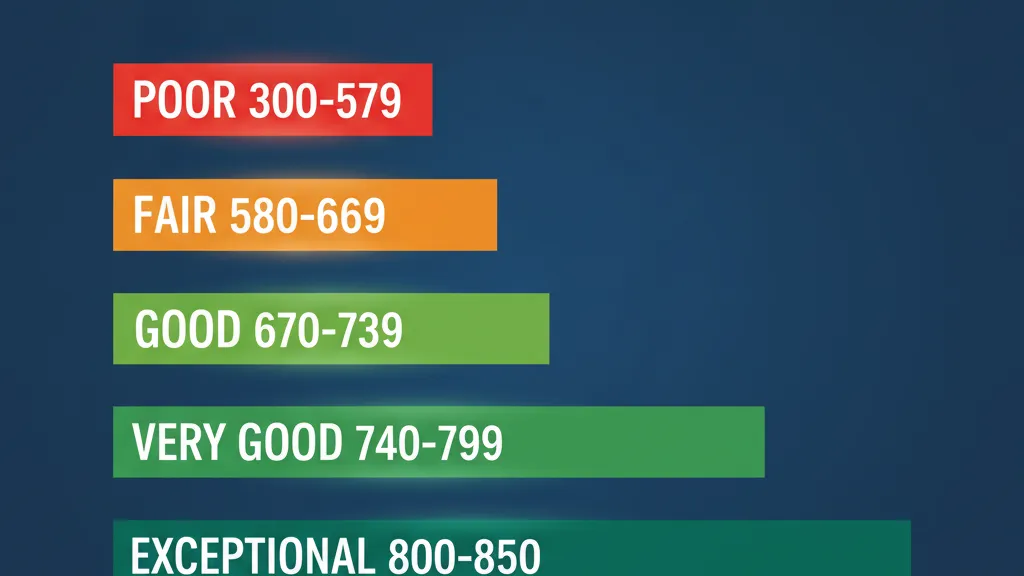

FICO Credit Score Ranges

| Score Range | Rating | What It Means |

|---|---|---|

| 800–850 | Exceptional | Best interest rates, instant approvals, access to elite rewards cards |

| 740–799 | Very Good | Near-top rates, strong approval odds for most products |

| 670–739 | Good | Qualifies for most mainstream credit products at competitive rates |

| 580–669 | Fair | Limited options, higher interest rates, may need a co-signer |

| 300–579 | Poor | Mostly secured cards and credit-builder loans; rebuilding required |

VantageScore Ranges

| Score Range | Rating |

|---|---|

| 781–850 | Excellent |

| 661–780 | Good |

| 601–660 | Fair |

| 500–600 | Poor |

| 300–499 | Very Poor |

The average FICO score in the United States reached approximately 715 in late 2025, according to Experian’s Consumer Credit Review. That places the typical American squarely in the “good” range.

What Is Considered a Good Credit Score?

A good credit score falls between 670 and 739 on the FICO scale. If your score lands here, you are viewed as a reliable borrower by most lenders. You will typically qualify for:

- Credit cards with competitive APRs and rewards programs

- Auto loans with favorable interest rates

- Personal loans without a co-signer

- Apartment rentals without extra deposits

However, “good” is relative to your financial goals. Here is what different milestones typically require:

Credit Score Requirements by Financial Goal

| Financial Goal | Minimum Score Needed | Ideal Score |

|---|---|---|

| Conventional mortgage | 620 | 740+ |

| FHA mortgage | 580 (3.5% down) | 680+ |

| Auto loan (prime rate) | 661 | 720+ |

| Premium rewards credit card | 670 | 740+ |

| Apartment rental | 620 | 670+ |

| Personal loan (best rates) | 670 | 720+ |

| Small business loan | 680 | 720+ |

The key takeaway: while a 670 score opens many doors, pushing above 740 unlocks the best rates and terms on virtually every financial product.

Is 700 a Good Credit Score?

Yes. A 700 credit score is firmly in the “good” range on the FICO scale. With a 700, you can expect:

- Mortgage approval at competitive rates (though not the absolute lowest)

- Auto loan approval at near-prime rates

- Credit card approval for most mainstream cards, including some rewards cards

- Lower insurance premiums in states that factor credit into pricing

A 700 score puts you ahead of roughly 40% of American consumers. It is a strong foundation, but there is still meaningful room to improve. Understanding how long it takes to improve your credit score can help you set realistic expectations and build an effective plan. Pushing from 700 to 740 or higher can save you a significant amount in interest, especially on large loans like mortgages. For more details, see our guide on establish business credit for your LLC.

For context, on a 30-year, $350,000 mortgage, the difference between a 700 and a 740 credit score could mean paying $30,000 to $50,000 less in total interest over the life of the loan.

See where you stand. Get your free credit analysis from M1 Credit Solutions

The Five Factors That Determine Your Credit Score

Understanding what goes into your score is the first step toward improving it. FICO scores are calculated using five weighted factors:

1. Payment History (35%)

This is the single most important factor. Lenders want to know if you pay your bills on time. Even one late payment of 30 days or more can drop your score by 50 to 100 points, depending on your starting score.

What helps: Consistent, on-time payments on all accounts including credit cards, loans, and utilities.

What hurts: Late payments, accounts in collections, bankruptcies, and foreclosures.

2. Amounts Owed / Credit Utilization (30%)

Credit utilization measures how much of your available credit you are using. Keeping your utilization below 30% is the general guideline, but below 10% is ideal for the highest scores.

Example: If you have a $10,000 total credit limit and carry a $2,500 balance, your utilization is 25%.

What helps: Low balances, high credit limits, paying balances before the statement date.

What hurts: Maxed-out cards, closing old accounts (which reduces available credit).

3. Length of Credit History (15%)

Longer credit histories generally produce higher scores. This factor considers the age of your oldest account, the age of your newest account, and the average age of all accounts.

What helps: Keeping old accounts open, even if you rarely use them.

What hurts: Closing long-standing accounts, opening many new accounts at once.

4. New Credit / Hard Inquiries (10%)

Each time you apply for credit, a hard inquiry appears on your report. Multiple hard inquiries in a short period can signal risk to lenders.

What helps: Spacing out credit applications, rate-shopping within a 14 to 45-day window (counted as one inquiry for mortgages and auto loans).

What hurts: Applying for several credit cards in quick succession.

5. Credit Mix (10%)

Lenders like to see a healthy mix of credit types: revolving credit (credit cards), installment loans (auto loans, mortgages), and retail accounts.

What helps: Having a diverse portfolio of credit types managed responsibly.

What hurts: Relying on only one type of credit.

For a deeper dive into each of these factors, read our guide on what affects your credit score.

Good Credit Score for Buying a House

A credit score of 670 or higher qualifies you for most mortgage products, but the score you need depends on the loan type:

- Conventional loans typically require a minimum score of 620, but you will need 740+ to secure the best interest rates.

- FHA loans accept scores as low as 580 with 3.5% down, or 500 with 10% down.

- VA loans have no official minimum, but most lenders look for 620+.

- USDA loans generally require 640+.

How Your Score Affects Mortgage Rates

The financial impact of your credit score on a mortgage is substantial. Here is an approximate comparison based on a $350,000, 30-year fixed-rate mortgage:

| Credit Score Range | Estimated APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 760–850 | 6.5% | $2,212 | $446,320 |

| 700–759 | 6.7% | $2,261 | $463,960 |

| 680–699 | 6.9% | $2,311 | $481,960 |

| 660–679 | 7.1% | $2,361 | $499,960 |

| 620–659 | 7.5% | $2,447 | $530,920 |

Note: Rates are illustrative and vary by lender, market conditions, and other borrower factors.

The difference between a 760 score and a 620 score on this mortgage amounts to over $84,000 in additional interest over 30 years. That is the real cost of a lower credit score.

If you are planning to buy a home, start working on your score at least 6 to 12 months before applying. Our guide on how to improve your credit score can help you build a plan.

How to Get a Good Credit Score

Building or rebuilding your credit takes time, but the steps are straightforward. Here is a practical step-by-step guide to improve your credit rating with actionable steps you can take today:

Step 1: Check Your Credit Reports for Errors

Mistakes on credit reports are more common than you might think. A Federal Trade Commission study found that roughly 1 in 5 consumers had an error on at least one credit report. Request your free reports from AnnualCreditReport.com and review each one carefully.

Look for:

– Accounts you do not recognize

– Incorrect payment statuses

– Outdated negative items (most should fall off after 7 years)

– Wrong balances or credit limits

If you find errors, disputing them can lead to quick score improvements. Start with a check your credit report from all three bureaus to see exactly what they contain. M1 Credit Solutions’ AI-powered platform analyzes your credit reports from all three bureaus and generates customized dispute letters automatically, saving you hours of research and paperwork.

Step 2: Pay Every Bill on Time

Since payment history accounts for 35% of your score, this is the single most impactful habit you can build. Set up autopay or calendar reminders for every account.

Step 3: Lower Your Credit Utilization

Aim to keep your utilization below 30%, and ideally below 10%. Consistent building good credit habits make this process sustainable. Strategies include:

– Paying balances twice per month (before the statement date)

– Requesting credit limit increases

– Keeping old accounts open to maintain higher total limits

Read our full credit utilization guide for more strategies.

Step 4: Avoid Unnecessary Hard Inquiries

Only apply for credit when you genuinely need it. Each hard inquiry can lower your score by 5 to 10 points temporarily.

Step 5: Build a Longer Credit History

Keep your oldest accounts open and active. If you are new to credit, consider a secured credit card or a credit-builder loan to start establishing history.

Step 6: Dispute Inaccurate Negative Items

If your credit report contains errors, collections you do not owe, or outdated information, disputing those items can significantly raise your score. M1 Credit Solutions’ AI platform identifies these items automatically and generates bureau-specific dispute letters you can send immediately.

Start your free credit analysis with M1 Credit Solutions

Step 7: Diversify Your Credit Mix

If you only have credit cards, consider adding an installment loan. If you only have loans, a secured credit card can help round out your profile.

Average Credit Score in the United States

Where does the typical American stand? Here are the latest benchmarks:

- National average FICO score: 715 (Experian, late 2025)

- Average VantageScore: 673

Average Credit Score by Generation

| Generation | Average Score |

|---|---|

| Silent Generation (78+) | 760 |

| Baby Boomers (60–77) | 742 |

| Generation X (44–59) | 706 |

| Millennials (28–43) | 687 |

| Generation Z (18–27) | 676 |

Younger consumers tend to have lower scores primarily because of shorter credit histories and higher utilization rates, not necessarily worse financial habits. If you are a younger borrower working to build credit from scratch, you are not alone, and the strategies above will help you climb the ranges faster.

What Is the Highest Credit Score?

The highest credit score possible is 850 on both the FICO and VantageScore scales. About 1.7% of FICO scores reach a perfect 850, according to FICO data.

Here is the practical reality: you do not need an 850. Research from Experian shows that borrowers with scores of 780 and above generally qualify for the same top-tier rates and terms. Once you are above 760, additional points offer diminishing returns in terms of financial benefits.

That said, maintaining a high score provides a buffer. If your score dips temporarily due to a hard inquiry or a brief utilization spike, you will still stay in the top tier.

How to Check Your Credit Score

Knowing your score is the first step toward improving it. Here are free ways to check:

- AnnualCreditReport.com – Free credit reports from all three bureaus (Experian, Equifax, TransUnion) once per year.

- Your bank or credit card issuer – Many financial institutions provide free FICO or VantageScore access.

- Free monitoring apps – Services like those from major bureaus offer ongoing score tracking.

- M1 Credit Solutions – Connect your credit reports to our platform to see your scores from all three bureaus, identify negative items, and get a personalized improvement plan.

For a complete walkthrough, see our guide on how to check your credit score.

Frequently Asked Questions

What is considered a good credit score?

A good credit score is 670 to 739 on the FICO scale, which is used in approximately 90% of U.S. lending decisions. On the VantageScore scale, a good score ranges from 661 to 780. With a good score, you qualify for most mainstream credit products at competitive interest rates.

Is 700 a good credit score?

Yes, 700 is a good credit score. It falls within the FICO “good” range (670–739) and puts you ahead of roughly 40% of consumers. You will qualify for most credit cards, auto loans, and personal loans, though pushing above 740 can unlock even better rates.

What credit score do you need to buy a house?

Most conventional mortgage lenders require a minimum FICO score of 620. FHA loans accept scores as low as 580 with 3.5% down. However, for the best mortgage rates, aim for 740 or higher. A higher score can save you tens of thousands of dollars in interest over a 30-year loan.

What is the highest credit score possible?

The highest credit score is 850 on both the FICO and VantageScore scales. However, scores above 780 generally receive the same top-tier rates and terms, so a perfect 850 is not necessary for the best financial outcomes.

How long does it take to build a good credit score?

Building a good credit score from scratch typically takes 6 to 12 months of responsible credit use. If you are rebuilding after a negative event like a late payment or collection, improvement can take 3 to 6 months of consistent positive behavior. Disputing inaccurate items on your credit report can sometimes produce results within 30 to 45 days.

Does checking my credit score lower it?

No. Checking your own credit score is a “soft inquiry” and does not affect your score. Only “hard inquiries” from lender-initiated credit applications can temporarily lower your score by a few points.

Take Control of Your Credit Score Today

Understanding credit score ranges is important, but taking action is what actually moves your score. Whether you are working to cross from “fair” to “good” or pushing from “good” to “excellent,” the steps are the same: pay on time, keep utilization low, dispute errors, and build a strong credit history.

If your credit report contains inaccurate or outdated negative items, you do not have to tackle the dispute process alone. M1 Credit Solutions’ AI-powered credit repair platform connects to all three bureaus, identifies items hurting your score, and generates customized dispute letters in minutes. It is the fastest, most affordable way to take control of your credit.

Start repairing your credit with M1 Credit Solutions

This article is for educational purposes only and does not constitute financial advice. Consult a qualified financial professional for guidance specific to your situation.