The credit score you need to buy a house depends on the mortgage program, the lender, and the rest of your application. This guide helps you compare common loan-program minimums and identify which options may fit your current credit profile.

Use the loan-type sections below to review FHA, conventional, VA, and USDA eligibility considerations before you speak with a lender.

If you already meet a loan minimum and want to strengthen your potential rate and terms, see what counts as a good credit score for a mortgage.

Minimum Credit Scores by Loan Type: A Quick Overview

Different mortgage programs have different credit score requirements. Here is a summary of what you need to know before you start shopping for a home:

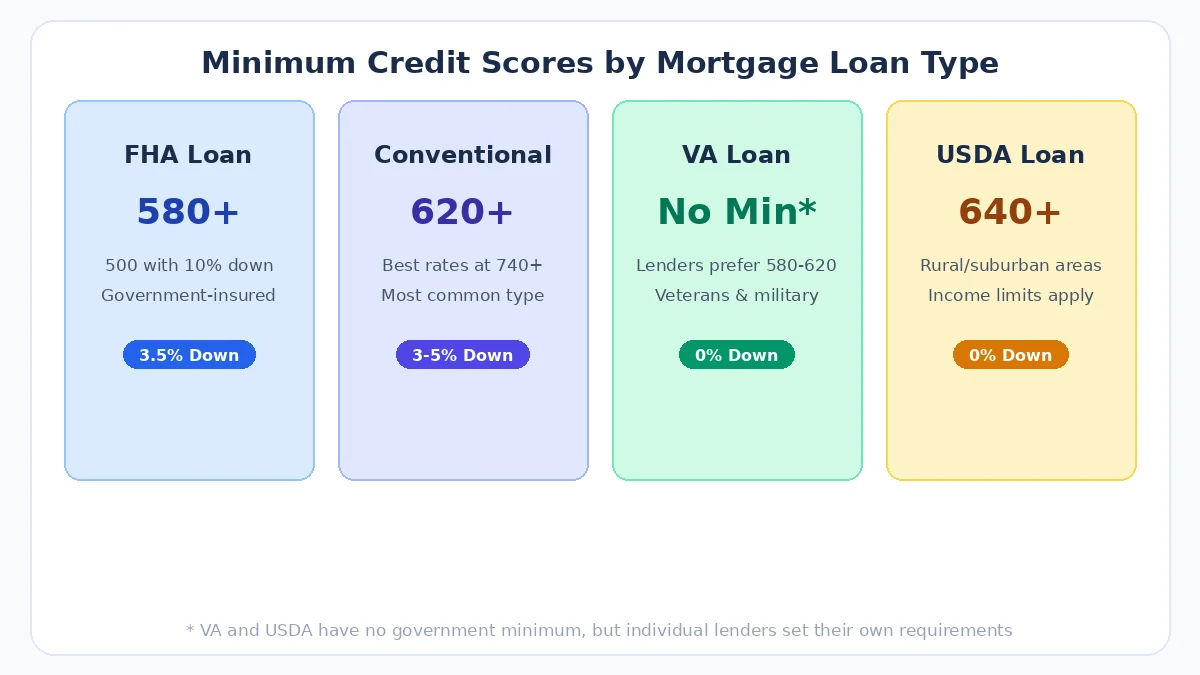

| Loan Type | Minimum Credit Score | Down Payment | Best For |

|---|---|---|---|

| FHA Loan | 580 (or 500 with 10% down) | 3.5% | First-time buyers and lower credit scores |

| Conventional Loan | 620 | 3%–5% | Buyers with solid credit and savings |

| VA Loan | No official minimum (lenders prefer 580–620) | 0% | Eligible veterans and military members |

| USDA Loan | No official minimum (lenders prefer 640) | 0% | Buyers in eligible rural areas |

| Jumbo Loan | 680–720+ | 10%+ | Higher-priced properties |

Now let us break down each loan type in detail so you know exactly where you stand.

FHA Loan Credit Score Requirements

FHA loans are insured by the Federal Housing Administration and are one of the most accessible mortgage options for buyers with lower credit scores. They are a popular choice for first-time home buyers.

Key requirements:

- Credit score of 580 or higher: You qualify for the minimum 3.5% down payment. On a $300,000 home, that is just $10,500 down.

- Credit score between 500 and 579: You may still qualify, but you need a 10% down payment. On that same $300,000 home, you would need $30,000 down.

- Credit score below 500: You will not qualify for an FHA loan.

What else to know about FHA loans:

- FHA loans require mortgage insurance premiums (MIP), including an upfront premium of 1.75% of the loan amount and an annual premium of 0.15% to 0.75%.

- If you put less than 10% down, MIP lasts for the life of the loan.

- FHA loan limits vary by county. In 2026, they range from approximately $541,287 in low-cost areas to $1,249,125 in high-cost areas.

- Many lenders apply their own “overlays,” meaning they may require a credit score slightly higher than the FHA minimum.

FHA loans are an excellent option if your credit score is below 620 but you have steady income and can afford the down payment. If your credit score is on the lower end, consider taking steps to improve it before applying so you can access the lower down payment option.

Conventional Loan Credit Score Requirements

Conventional loans are the most common type of mortgage in the United States. They are not backed by a government agency but follow rules set by Fannie Mae and Freddie Mac.

Key requirements:

- Minimum credit score: 620. This is the standard threshold most lenders use.

- Down payment: 3% to 5% for most borrowers, though 20% down eliminates private mortgage insurance (PMI).

- Best rates available at 740+: Borrowers with scores of 740 or higher receive the most competitive interest rates and lowest PMI premiums.

What else to know about conventional loans:

- PMI is required when you put less than 20% down. It typically costs between 0.58% and 1.86% of the loan amount annually.

- PMI can be removed once you reach 20% equity, unlike FHA mortgage insurance which often lasts the life of the loan.

- Conforming loan limits for 2026 are $832,750 in most areas and up to $1,249,125 in high-cost areas.

- Debt-to-income (DTI) ratio should be 45% or lower.

If you are looking to improve your credit score fast to qualify for a conventional loan, even a 20- to 40-point increase can make a meaningful difference in your approval odds and interest rate.

VA Loan Credit Score Requirements

VA loans are backed by the U.S. Department of Veterans Affairs and are available to eligible veterans, active-duty service members, and qualifying surviving spouses.

Key requirements:

- No official minimum credit score. The VA does not set a minimum score requirement.

- Most lenders prefer 580 to 620. In practice, you will need at least this range for approval.

- Zero down payment required in most cases.

- No monthly mortgage insurance. VA loans charge a one-time funding fee of 2.15% to 3.30% instead.

What else to know about VA loans:

- VA loans have no loan limit for borrowers with full entitlement.

- Lenders evaluate the full financial picture, including residual income and employment history.

- VA loans offer some of the best terms available for qualifying borrowers, making them an excellent choice if you are eligible.

Even without a strict minimum, having a higher credit score gives you more lender options and better rates. If you are a veteran preparing to buy a home, focus on fixing any credit issues well before you apply.

USDA Loan Credit Score Requirements

USDA loans are backed by the U.S. Department of Agriculture and are designed for moderate- to low-income buyers purchasing homes in eligible rural and suburban areas.

Key requirements:

- No official minimum credit score. Like VA loans, USDA does not publish a required score.

- Most lenders require 640 or higher for automated approval through their systems.

- Below 640: You may still qualify through manual underwriting, but the process is longer and more detailed.

- Zero down payment required.

What else to know about USDA loans:

- USDA loans have income limits based on your area and household size.

- They charge an upfront guarantee fee of 1% and an annual fee of 0.35%.

- The property must be in a USDA-eligible rural area and must be your primary residence.

USDA loans offer an incredible opportunity for buyers who qualify. If your score is just below 640, improving it by even a small amount can streamline the approval process.

Meeting the Minimum vs. Getting Better Mortgage Terms

Meeting a mortgage program’s minimum credit requirement may help establish eligibility, but it does not guarantee a particular approval, rate, or loan term. Once you understand which programs may fit your score, compare your full credit profile and options with qualified lenders. Use the mortgage-score guide linked above when your goal shifts from meeting a minimum to pursuing stronger terms.

How Your Credit Score Affects Your Down Payment

Your credit score also affects how much you need for a down payment, particularly with FHA and conventional loans:

- FHA with 580+ score: 3.5% down ($10,500 on a $300,000 home)

- FHA with 500–579 score: 10% down ($30,000 on a $300,000 home)

- Conventional with 620+ score: 3% to 5% down

- VA and USDA loans: 0% down regardless of score (but lender overlays may apply)

A higher credit score gives you access to lower down payment options, which means you need less cash upfront to become a homeowner. If you are working to build better credit for loans, the payoff goes beyond just the interest rate.

What Credit Score Model Do Mortgage Lenders Use?

This is an important detail many buyers miss. Mortgage lenders do not use the same credit score you see on free monitoring apps. Most mortgage lenders use FICO scores, specifically:

- FICO Score 2 (Experian)

- FICO Score 5 (Equifax)

- FICO Score 4 (TransUnion)

Lenders pull your score from all three bureaus and typically use the middle score for qualification. If you are applying with a co-borrower, the lender usually uses the lower of the two middle scores.

Your FICO mortgage score may be different from your VantageScore (used by Credit Karma and many free tools), sometimes by 20 points or more. This is why it is critical to check your actual credit reports and identify any errors or negative items that may be dragging your score down.

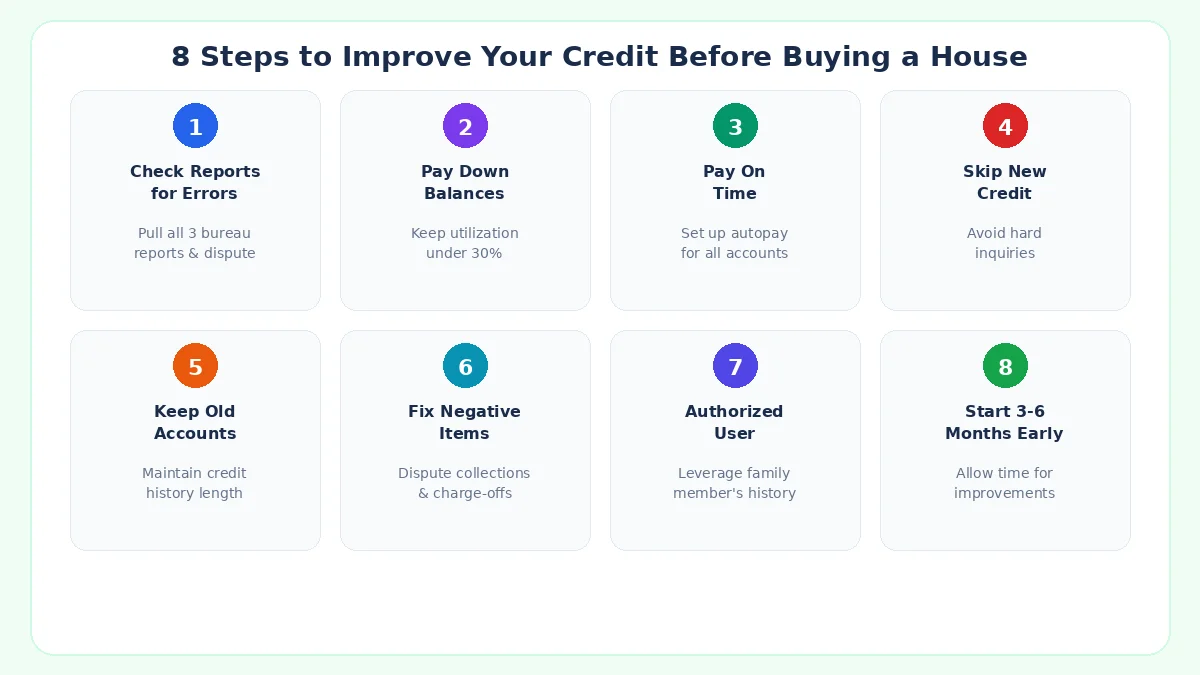

8 Steps to Improve Your Credit Score Before Buying a House

If your credit score is not quite where it needs to be, do not worry. With the right strategy, you can improve your credit score significantly in a matter of months. Here are proven steps to get mortgage-ready:

1. Pull Your Credit Reports and Check for Errors

Start by getting free copies of your credit reports from all three bureaus at AnnualCreditReport.com, then check your credit reports for errors. Look for:

- Incorrect late payments

- Accounts that do not belong to you

- Wrong balances or credit limits

- Duplicate collection accounts

Errors are more common than you might think, and disputing them can produce quick score improvements. M1 Credit Solutions’ AI-powered platform connects to all three credit bureaus, identifies negative items automatically, and generates custom dispute letters tailored to your situation.

2. Pay Down Credit Card Balances

Your credit utilization ratio (the amount of credit you use compared to your total available credit) accounts for about 30% of your FICO score. For the best results:

- Keep individual card utilization below 30%

- Aim for below 10% for maximum score impact

- Pay balances down before your statement closing date so the lower balance gets reported

3. Make Every Payment on Time

Payment history is the single most important factor in your credit score, accounting for 35% of your FICO score. Set up autopay for at least the minimum payment on every account to avoid late payments.

4. Do Not Open New Credit Accounts

Every time you apply for new credit, it creates a hard inquiry on your report, which can temporarily lower your score by 5 to 10 points. In the months before applying for a mortgage:

- Avoid applying for new credit cards

- Do not finance furniture or appliances

- Do not co-sign for anyone else

5. Do Not Close Old Credit Accounts

The length of your credit history matters. Closing an old account can:

- Reduce your average account age

- Lower your total available credit (increasing utilization)

Keep old accounts open, even if you are not using them regularly.

6. Address Collections and Negative Items

Collections, charge-offs, and other derogatory marks can significantly lower your score. You have options:

- Dispute inaccurate items with the credit bureaus

- Negotiate pay-for-delete agreements with collection agencies

- Request goodwill removals for isolated late payments

This is where a structured approach to DIY credit repair makes a real difference. Rather than guessing which items to dispute or what language to use, a guided platform walks you through the process step by step.

7. Become an Authorized User

If a family member has a credit card with a long positive history and low utilization, ask to be added as an authorized user. Their positive payment history can boost your score without requiring you to use the card.

8. Give Yourself Time

Most credit improvements take 30 to 90 days to show up on your reports. If possible, start working on your credit at least 3 to 6 months before you plan to apply for a mortgage. The earlier you start, the more options you will have when it is time to buy.

Can You Buy a House with Bad Credit?

Yes, you can buy a house with bad credit, but your options are more limited and more expensive. Here is what to expect:

- 500–579 credit score: Your only standard option is an FHA loan with 10% down. Expect higher interest rates and limited lender choices.

- 580–619 credit score: You qualify for FHA loans with 3.5% down and may be eligible for some VA programs. Rates will be above average.

- 620–659 credit score: You can access conventional loans, but rates and PMI costs will be higher.

- 660+ credit score: You begin to access more competitive rates and more loan options.

Buying with bad credit means paying more over the life of your loan. If you can improve your score by even 40 to 60 points before applying, the savings can be substantial, often tens of thousands of dollars.

How Long Does It Take to Build Your Credit Score for a Mortgage?

The timeline depends on your starting point and what is affecting your score:

| Situation | Typical Timeline |

|---|---|

| Paying down high credit card balances | 1–2 billing cycles (30–60 days) |

| Disputing errors on your credit report | 30–45 days per dispute round |

| Recovering from a late payment | 3–6 months of on-time payments |

| Rebuilding after collections removal | 1–3 months for score to update |

| Recovering from bankruptcy | 1–2 years of active rebuilding |

Starting early gives you the most leverage. If you are thinking about buying a home in the next 6 to 12 months, now is the time to start improving your credit score.

Improve Your Credit to Meet a Home Loan Minimum

If credit-report errors or negative items are keeping you below a loan-program minimum, M1 Credit Solutions can help you review your reports and take a more organized, do-it-yourself approach to improving your credit profile.

Here is how it works:

- Connect your credit reports from all three bureaus (Experian, Equifax, and TransUnion) in minutes.

- AI identifies negative items that are hurting your score, including collections, late payments, charge-offs, and errors.

- Generate custom dispute letters with language tailored to your specific situation, not generic templates.

- Track your progress with a real-time dashboard that shows your score changes and dispute statuses.

Whether you need to boost your score by 20 points to qualify for a conventional loan or 80 points to reach FHA eligibility, M1 Credit Solutions gives you a clear, step-by-step path to get there. Start your credit repair journey today.

Frequently Asked Questions

What is the minimum credit score to buy a house?

The minimum credit score depends on the loan type. FHA loans allow scores as low as 500 with a 10% down payment, or 580 with 3.5% down. Conventional loans typically require 620. VA and USDA loans have no government-mandated minimum, but most lenders prefer scores of 580 to 640.

Can I buy a house with a 580 credit score?

Yes. With a 580 credit score, you can qualify for an FHA loan with as little as 3.5% down. Some VA lenders also accept scores in this range. However, your interest rate will be higher than if you had a score of 700 or above.

What credit score do I need for a conventional loan?

Most conventional loan lenders require a minimum credit score of 620. For the best interest rates and lowest PMI costs, aim for a score of 740 or higher.

How much does your credit score affect your mortgage rate?

Significantly. A borrower with a 760+ score might pay 6.50% interest, while someone with a 620 score could pay 8% or more. On a $300,000 loan over 30 years, that difference adds up to over $100,000 in extra interest.

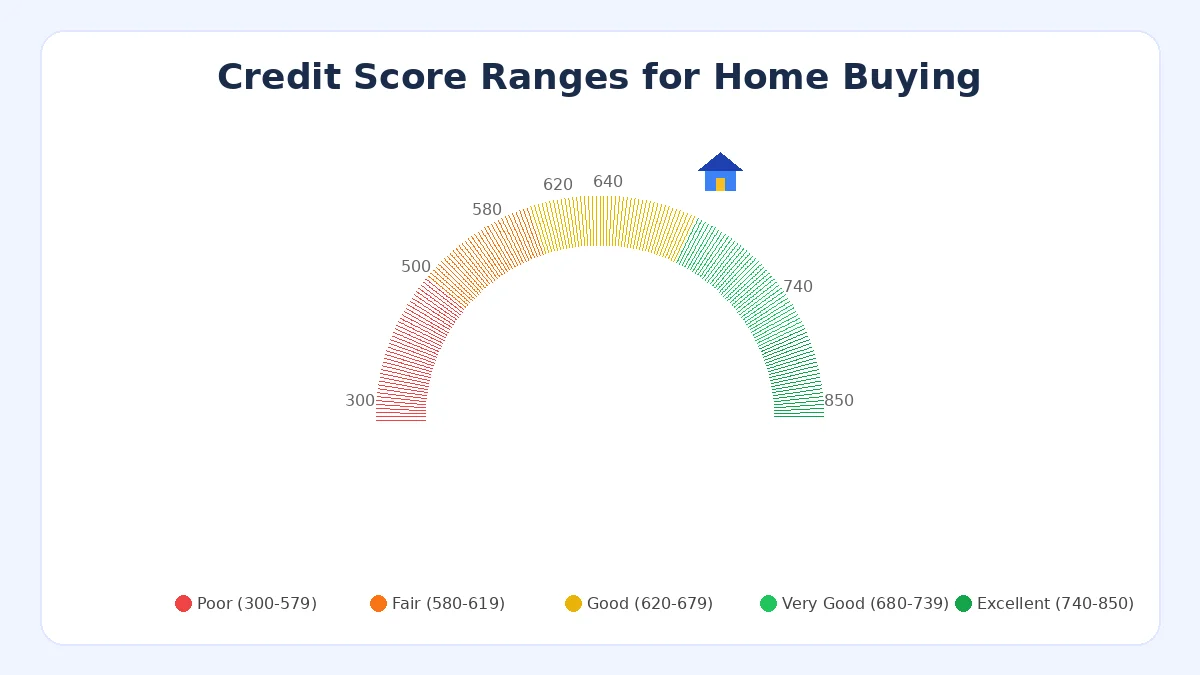

What is a good credit score to buy a house?

A credit score of 670 or higher is generally considered “good” for home buying. Scores of 740 and above are considered “very good” to “excellent” and qualify you for the best mortgage rates and terms.

Do mortgage lenders use FICO or VantageScore?

Most mortgage lenders use FICO scores, specifically FICO Score 2 (Experian), FICO Score 5 (Equifax), and FICO Score 4 (TransUnion). The score you see on free monitoring apps may differ from what your lender uses.

How long before buying a house should I start improving my credit?

Ideally, start at least 3 to 6 months before you plan to apply for a mortgage. This gives you time to dispute errors, pay down balances, and see the improvements reflected on your credit reports.

Can I get a mortgage with no credit history?

It is difficult but possible. FHA and USDA loans allow for manual underwriting, where lenders evaluate your financial history through alternative means like rent payments, utility bills, and insurance payments. However, having an established credit history makes the process much easier.