If you are trying to qualify for a mortgage or auto loan, the difference between a rapid rescore and credit repair can decide whether you need a few days, a full billing cycle, or several months to improve your credit profile. Both can help your credit report reflect better information, but they are not the same tool. Rapid rescoring is usually handled by a lender to update verified account changes quickly. Credit repair is a longer process focused on disputing inaccurate, unverifiable, or outdated items and building healthier credit habits over time.

Need a longer-term credit improvement plan before your next major loan? M1 Credit Solutions gives you AI-powered tools to review your credit, create dispute letters, and manage your own credit repair process for $29.99/month.

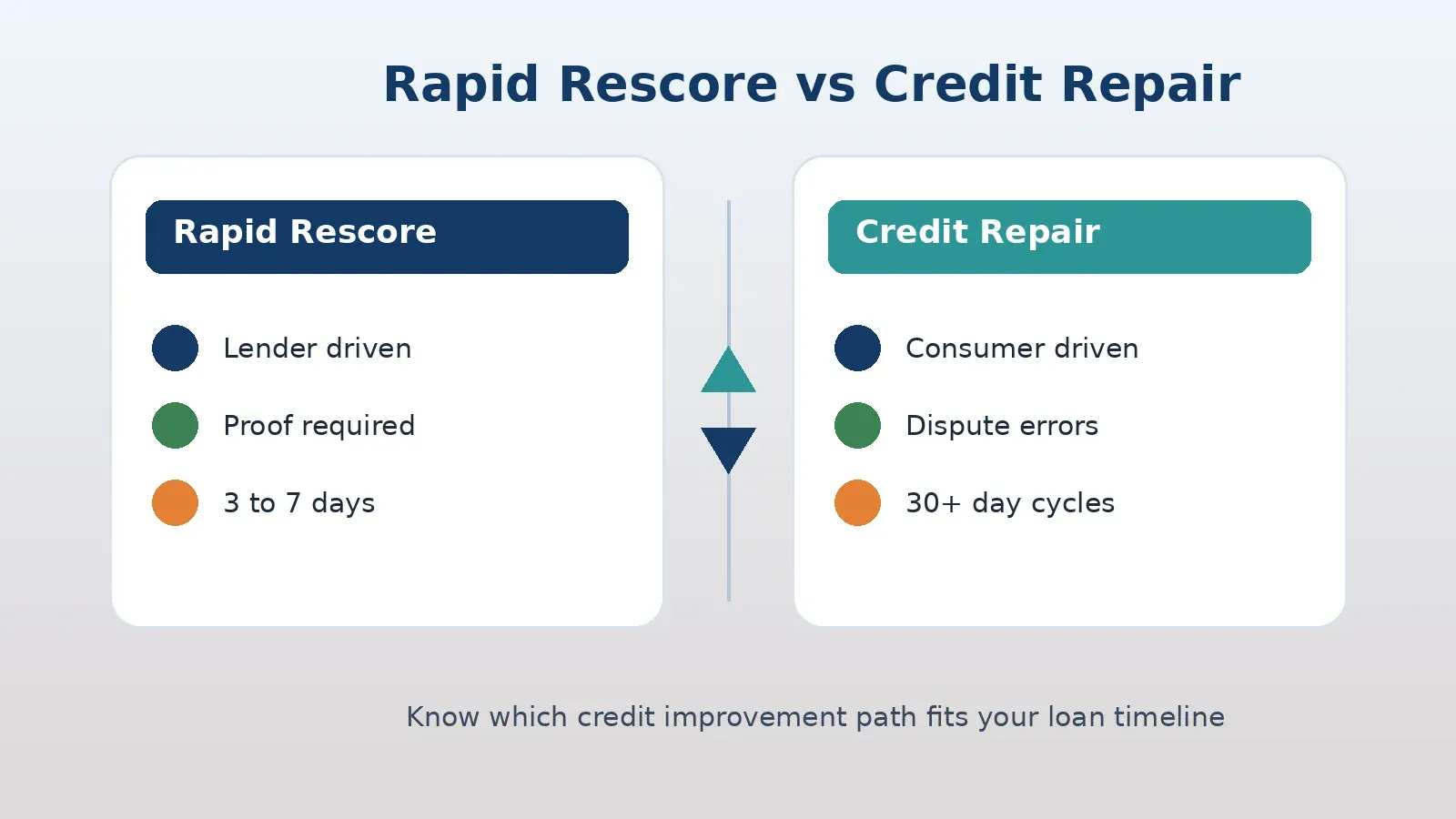

This guide compares rapid rescore vs credit repair in plain English, including how each works, who controls the process, what timelines to expect, and which option fits a mortgage or auto-loan deadline.

Quick Answer: Rapid Rescore vs Credit Repair

A rapid rescore is a lender-driven request to update your credit report quickly after you have proof of a specific change, such as a paid-down credit card balance or a corrected reporting error. Credit repair is a consumer-driven process of reviewing credit reports, disputing inaccurate information, and improving the habits that affect your score over time.

| Factor | Rapid Rescore | Credit Repair |

|---|---|---|

| Main purpose | Update recent verified changes quickly | Challenge inaccurate items and improve credit over time |

| Who usually starts it | Your mortgage or auto lender | You, or a credit repair service or DIY platform |

| Typical timeline | Often a few business days after proof is submitted | Usually 30 days or more per dispute cycle |

| Best for | A near-term loan approval or rate threshold | Longer-term credit report improvement |

| What it cannot do | Erase accurate negative history | Guarantee a score increase or instant loan approval |

What Is a Rapid Rescore?

A rapid rescore is a process lenders use to ask the credit bureaus to update your credit report faster than the normal reporting cycle. It is most common during mortgage underwriting, but some auto lenders may use similar update processes when a borrower is close to qualifying or close to a better pricing tier.

The key detail is control. A rapid rescore is not something you usually order on your own as a consumer. Your lender or loan officer reviews your credit report, identifies a specific item that could change your score, collects proof, and submits the update request through the lender’s credit reporting provider.

For example, say your mortgage credit score is 718, but your lender says a 720 score could help you qualify for a better rate. If one credit card still reports a high balance even though you already paid it down, the lender may ask for proof of the new balance and request a rapid rescore. If the update is accepted and the scoring model responds as expected, your score may refresh quickly enough to help with the loan file.

Rapid rescoring works best when the change is simple, documented, and already completed. It is not a magic score booster. It does not create new credit history, remove accurate late payments, or replace the work of improving your full credit profile.

What Is Credit Repair?

Credit repair is the process of reviewing your credit reports and disputing information that may be inaccurate, incomplete, outdated, duplicated, or unverifiable. It can include disputes with Equifax, Experian, TransUnion, creditors, and collection agencies. It can also include practical score-building steps, such as lowering utilization, managing payment dates, and checking your reports regularly.

Credit repair can be handled in different ways. Some people send disputes directly to the credit bureaus on their own. Others hire a traditional agency. M1 Credit Solutions takes a DIY approach by giving users AI-powered tools to analyze reports and generate customized dispute letters while keeping control in the consumer’s hands.

If you are new to disputes, start with the basics. Review how to check your credit report for free, then look for items that should be corrected before you apply for a major loan. Errors involving payment history, collections, balances, account ownership, and identity mix-ups can all create serious problems if they remain on your file.

Credit repair is slower than rapid rescoring because disputes follow investigation timelines. A bureau or furnisher generally needs time to review the dispute and respond. That means credit repair is better for planning ahead, not for trying to fix a loan file the week before closing.

How Rapid Rescoring Works

The rapid rescore process usually starts after a lender pulls your credit and sees a clear opportunity. The loan officer may run a credit simulation to estimate what could happen if a balance is updated, an account is corrected, or a reporting error is fixed. If the change could help you qualify or improve pricing, the lender explains what documentation is needed.

Common rapid rescore steps

- The lender reviews your credit file. This is usually part of a mortgage preapproval, underwriting review, or loan pricing discussion.

- A specific update is identified. The lender might focus on a recently paid-down credit card, a corrected collection balance, or an account that is reporting wrong information.

- You provide proof. This may include a creditor letter, account statement, payoff confirmation, or balance update showing the new information.

- The lender submits the request. The request goes through the lender’s credit reporting system, not directly from you to the bureau.

- The credit report and score are refreshed. If the update is accepted, the lender can pull an updated report and use the new score in the loan process.

Because the lender controls the request, ask early if rapid rescoring is available. Not every lender offers it, and not every credit issue qualifies. It is also important to confirm whether the projected score change would actually help your loan approval, rate, or mortgage insurance cost.

How Credit Repair Works

Credit repair starts before the lender is involved. The goal is to clean up inaccurate reporting and build a stronger credit foundation so you are not relying on a last-minute update. This is why credit repair often matters most three to twelve months before a mortgage, auto loan, apartment application, or business funding request.

Common credit repair steps

- Pull all three credit reports. Your Equifax, Experian, and TransUnion reports may not match. A problem on one bureau can still affect a lender’s decision.

- Review high-impact errors first. Focus on late payments, collections, charge-offs, incorrect balances, mixed files, duplicate accounts, and accounts that do not belong to you.

- Create targeted disputes. A strong dispute should explain what is wrong, identify the account clearly, and include supporting documents when available.

- Track responses and deadlines. Keep copies of letters, documents, investigation results, and follow-up dates.

- Improve the score factors you can control. Pay on time, reduce revolving balances, avoid unnecessary hard inquiries, and keep older positive accounts in good standing.

M1 Credit Solutions is built for this longer-term path. Instead of paying a traditional agency to work behind the scenes, users can review their own credit situation, use AI-powered dispute letter generation, and stay involved in every step of the process.

Want help deciding which credit report errors to tackle first? Use M1 Credit Solutions to organize your report review and create dispute letters you can send yourself.

When a Rapid Rescore Makes Sense

A rapid rescore makes the most sense when you are already in a loan process and a specific update could make a measurable difference. It is especially useful when your score is close to a cutoff.

Mortgage borrowers often face score thresholds that affect approval, interest rate, private mortgage insurance, and loan program options. If you are preparing to buy a home, read what lenders consider a good credit score for a mortgage so you understand why a few points can matter.

Good rapid rescore scenarios

- You paid down a credit card, but the lower balance has not reported yet.

- A creditor corrected an error and gave you written proof.

- You are just below a lender’s score requirement.

- You are close to a better interest rate or mortgage insurance tier.

- Your loan timeline cannot wait for the next regular reporting cycle.

Rapid rescoring can be powerful in these situations because it compresses the update timeline. It does not guarantee that your score will rise, but it can help your report reflect current verified information faster.

When Credit Repair Makes Sense

Credit repair makes more sense when the problem is broader than one recent update. If your report has old collections, questionable late payments, duplicate accounts, charge-offs, incorrect personal information, or accounts you do not recognize, you need a structured review instead of a single rescore request.

For example, a borrower with several inaccurate collections may not benefit from a rapid rescore unless those items have already been corrected and proof is available. A better starting point would be learning which credit report errors to dispute first, then building a dispute plan that targets the items most likely to affect approval.

Good credit repair scenarios

- You are months away from applying for a mortgage, auto loan, or business loan.

- You see accounts, balances, or late payments that appear inaccurate.

- You need to understand and document your dispute history.

- You want to lower utilization before a lender pulls your credit.

- You want a lower-cost alternative to traditional credit repair agencies.

Credit repair can also support small business owners whose personal credit affects funding options. If your personal credit is holding back a business loan, equipment financing, or business credit card application, improving the underlying report may help you approach lenders from a stronger position.

Paydowns, Disputes, and Report Updates: Which Path Fits?

The right option depends on what needs to change. Many borrowers use the wrong phrase when they say they need to “fix” their credit quickly. Sometimes they need a balance update. Sometimes they need a dispute. Sometimes they need a longer score-building plan.

| Situation | Best starting point | Why |

|---|---|---|

| You paid a credit card down yesterday | Ask your lender about rapid rescore | The lower balance may not show until the next reporting cycle unless the lender can request an update. |

| A collection is not yours | Credit repair dispute | The issue must be investigated and corrected before a rescore can reflect anything new. |

| Your utilization is high across several cards | Paydown strategy, then possible rescore | Lower balances can help, but the new balances need to report or be documented for a lender. |

| You have several old negative items | Credit repair plan | There is no single quick update. You need review, disputes where appropriate, and time. |

| You are two points below a loan threshold | Lender review, then rapid rescore if eligible | A lender can tell whether a specific update could move the loan file forward. |

Utilization is one of the most common areas where borrowers confuse the two paths. Paying down credit cards may improve your score, but only after the new balances reach the credit bureaus or are processed through a lender-driven update. For a deeper explanation, read how credit utilization affects your credit score.

Can Credit Repair Replace a Rapid Rescore?

Credit repair cannot replace a rapid rescore when the immediate need is a lender-controlled update during underwriting. If you already have proof that a balance or correction should be reflected now, the fastest route is usually to ask the lender whether a rapid rescore is possible.

But rapid rescoring cannot replace credit repair either. If negative items are inaccurate, outdated, or unverifiable, they need to be reviewed and disputed through the proper process. If your payment history, utilization, or account mix needs work, you need a longer plan. Rapid rescoring is about speed. Credit repair is about accuracy, control, and long-term improvement.

Think of it this way: rapid rescoring is a snapshot update for a loan decision, while credit repair is the process of improving the information behind the snapshot.

What Rapid Rescoring Cannot Do

Rapid rescoring has limits. It should not be treated as a shortcut around accurate credit history. If a late payment is accurate, a rescore will not make it disappear. If a collection is valid and still being reported correctly, the lender cannot simply remove it through rapid rescoring. If you have no documentation, there may be nothing to submit.

- It cannot remove accurate negative information.

- It cannot force a score increase.

- It cannot replace a full dispute process.

- It cannot create months of positive payment history.

- It cannot be ordered directly by most consumers.

It can also backfire if the updated report brings in new negative information or if the expected score change does not happen. Your lender should review the likely benefit before submitting a request.

What Credit Repair Cannot Do

Credit repair also has limits. No company or software platform can legally guarantee that your score will increase, that every negative item will be removed, or that you will qualify for a specific loan. Be careful with any service that promises instant results or claims it can delete accurate information.

A trustworthy credit repair process should focus on accuracy and documentation. If you are comparing dispute approaches, our guide to 609 dispute letters explains why the letter format matters less than the facts, records, and follow-up behind the dispute.

Credit repair works best when paired with healthy credit behavior. That means paying bills on time, keeping credit card balances low, avoiding unnecessary applications, and checking reports before major financial decisions. If you are unsure where your score stands, review the credit score chart to see how lenders may view your current range.

Best Timeline Before a Mortgage or Auto Loan

If you have not applied yet, start credit repair as early as possible. Three to six months gives you more room to review reports, send disputes, pay down balances, and let updates show naturally. Six to twelve months is even better if you have multiple negative items or thin credit history.

If you are already under contract for a home or sitting in a dealership finance office, the strategy changes. You do not have time for a full dispute cycle to play out before the decision. In that case, ask the lender whether a documented balance update or corrected account could support a rapid rescore.

A simple decision framework

- Applying in 6 months or more: Start credit repair and score-building now.

- Applying in 1 to 3 months: Review reports, lower utilization, avoid new hard inquiries, and dispute clear errors quickly.

- Already in underwriting: Ask the lender about rapid rescoring only for documented updates.

- Denied or priced too high: Get the adverse action reasons, review your reports, and build a repair plan before reapplying.

Hard inquiries can also affect timing. If you are rate shopping or preparing to apply, read how credit inquiries affect your score so you do not create avoidable score pressure while trying to improve your file.

How M1 Credit Solutions Fits Into the Process

M1 Credit Solutions is not a rapid rescoring service. Rapid rescoring is usually handled by lenders during a loan process. M1 Credit Solutions is designed for the longer-term side of the equation: helping consumers and small business owners understand their credit reports, generate customized dispute letters, and take control of their credit repair work.

That distinction matters. If your lender says a rapid rescore is available, follow the lender’s documentation instructions. If your report has deeper issues or you want to prepare before a lender pulls credit, use a DIY credit repair platform to organize the work earlier.

M1’s technology-first model is built around affordability and control. Instead of paying traditional credit repair agency prices, users can manage the process themselves with AI support for $29.99/month. That makes it a practical fit for people who want transparency, lower cost, and a repeatable system for reviewing and disputing credit report issues.

Ready to work on your credit before the loan deadline gets close? Get started with M1 Credit Solutions and build a credit improvement plan you control.

Common Questions About Rapid Rescore vs Credit Repair

Is rapid rescoring the same as credit repair?

No. Rapid rescoring is usually a lender-driven update request for verified credit report changes. Credit repair is a broader process of reviewing reports, disputing inaccurate items, and improving credit habits over time.

Can I request a rapid rescore myself?

Usually no. Rapid rescoring is typically requested by a mortgage lender, broker, bank, credit union, or similar lender through its credit reporting provider. Consumers can provide proof, but the lender usually submits the request.

How fast does a rapid rescore work?

Many rapid rescore requests are completed within a few business days after the lender has the right documentation, but timing varies by lender, credit bureau, furnisher, and the type of update.

How long does credit repair take?

Credit repair usually takes longer because disputes need investigation and follow-up. Some updates may happen within one dispute cycle, while more complex credit report problems can take several months.

Which is better before a mortgage?

If you are months away from applying, credit repair and utilization management are usually better starting points. If you are already in underwriting and have proof of a specific update, ask your lender whether a rapid rescore makes sense.

Bottom Line: Use the Right Tool for the Timeline

The rapid rescore vs credit repair decision comes down to timing, control, and proof. Rapid rescoring is best when a lender can document a specific update that may help a near-term loan file. Credit repair is best when you need to challenge inaccurate information, understand your reports, and improve your credit foundation before the pressure of an application.

If your loan deadline is days away, talk to your lender about whether rapid rescoring is available. If your goal is to qualify more confidently in the future, start reviewing your credit reports now. The earlier you begin, the more options you have.