Your credit score is a three-digit number that controls more of your financial life than your salary. It determines the interest rate on your mortgage, whether you get approved for that rewards credit card, and how much you pay for auto insurance. But the raw number only tells part of the story. What really matters is which tier your score falls into, because lenders make decisions based on ranges, not individual points.

📊 Know Your Credit Score Tier — Take Control Today

M1 Credit Solutions connects to all three credit bureaus, identifies negative items dragging your score down, and generates custom dispute letters using AI. Take the first step toward a higher tier.

This guide breaks down every credit score range across the full credit score scale for both FICO and VantageScore models, shows you exactly what each tier means for lending decisions, and provides a clear roadmap for moving up. Whether you are trying to qualify for a mortgage, get a better auto loan rate, or simply understand where you stand on the credit score ranges, this is the only credit score chart you need.

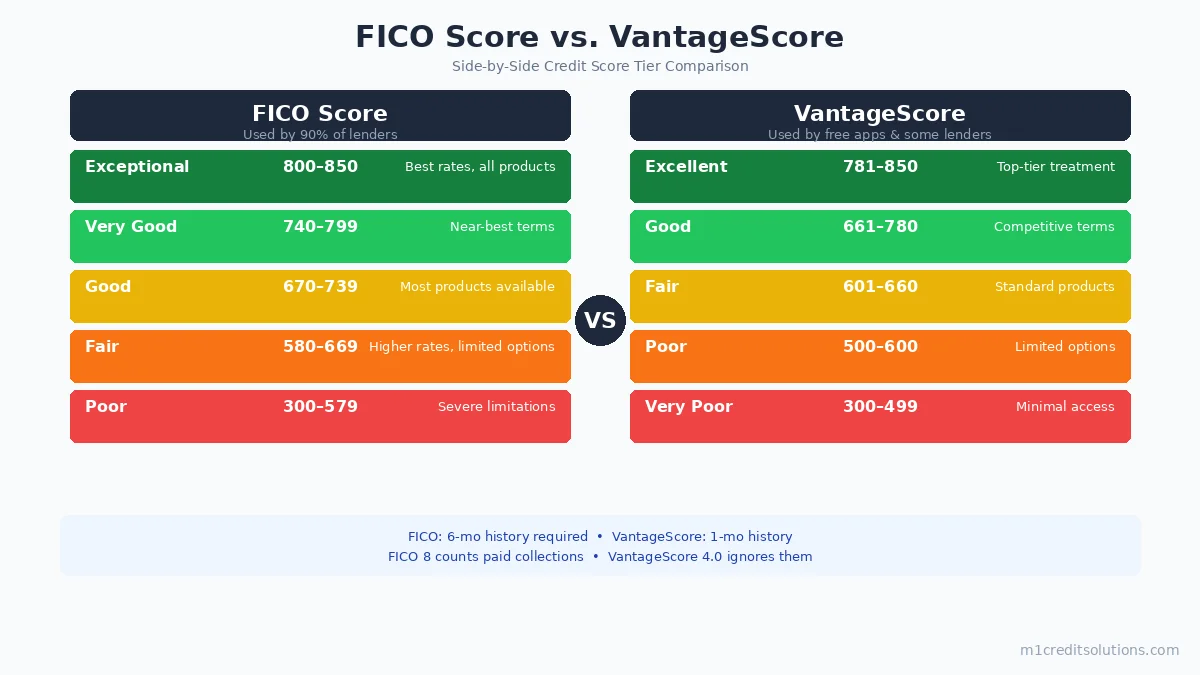

Credit Score Chart: FICO Score Ranges (300–850)

The FICO score is the gold standard in U.S. lending. Created by Fair Isaac Corporation in 1956, FICO is used in approximately 90% of all U.S. lending decisions, according to the company’s own filings. FICO scores range from 300 to 850 and are divided into five tiers.

Here is the complete FICO credit score chart:

| FICO Score Range | Rating | % of Americans | What It Means for You |

|---|---|---|---|

| 800–850 | Exceptional | ~24% | Best rates on everything. Lenders compete for your business. |

| 740–799 | Very Good | ~17% | Near-best terms. Approved for premium credit cards and lowest mortgage rates. |

| 670–739 | Good | ~21% | Considered an acceptable borrower. Access to most credit products at competitive rates. |

| 580–669 | Fair | ~18% | Subprime territory. Higher interest rates and limited product selection. |

| 300–579 | Poor | ~16% | Significant difficulty getting approved. Highest rates and most restrictive terms. |

Key stat: As of late 2025, the average FICO score in the United States is 715, placing the typical American in the “Good” tier. However, 71.2% of Americans now hold a FICO score of 670 or higher, according to FICO’s Credit Insights Report.

800–850: Exceptional Credit

If your score falls in this range, you are in the top tier of American credit consumers. Lenders view you as an extremely low default risk.

What this tier unlocks:

- Approval for virtually every credit card, including ultra-premium products like the Chase Sapphire Reserve and Amex Platinum

- The best available interest rates on mortgages, auto loans, and personal loans

- Highest credit limits offered by issuers

- Instant approvals on most applications

- Lowest auto insurance premiums (in states that use credit for pricing)

Typical behaviors at this level:

- Credit utilization under 7%

- No missed payments in 7+ years

- Average account age of 9+ years

- Mix of revolving and installment accounts

- Fewer than 3 hard inquiries in 24 months

740–799: Very Good Credit

You are a highly creditworthy borrower. The vast majority of credit products are accessible at near-best terms. The difference between this tier and Exceptional is minimal for most lending products.

What this tier unlocks:

- All major rewards credit cards

- Mortgage approval at rates typically within 0.125% of the best available

- Prime auto loan rates

- Favorable personal loan terms

- Easy rental approval in competitive markets

670–739: Good Credit

This is the threshold most lenders use as the floor for standard credit products. If your score is in this range, you are considered an acceptable borrower, though you will not receive the absolute best rates.

What this tier unlocks:

- Most mainstream credit cards (cashback, basic travel rewards)

- Conventional mortgage approval (minimum 620, but competitive rates start here)

- Standard auto loan rates

- Personal loan approval at moderate interest rates

Important note: Moving from the top of “Good” (739) to “Very Good” (740) can save you thousands of dollars over the life of a mortgage. The difference between a 3.5% and a 4.0% rate on a $350,000 mortgage is over $35,000 in total interest.

580–669: Fair Credit

Fair credit puts you in subprime territory. You can still get approved for some credit products, but expect to pay more for them.

What this tier means:

- FHA loan eligibility with 3.5% down payment (minimum 580)

- Higher interest rates on all products (1–3% above prime rates)

- Limited credit card options, often with annual fees and lower limits

- Security deposits may be required for utilities and cell phone plans

- Some landlords may require larger security deposits or co-signers

300–579: Poor Credit

A score in this range represents significant credit challenges. Mainstream lending options are severely limited.

What this tier means:

- Denied for most conventional credit products

- FHA loans possible with 500–579, but require 10% down payment

- Secured credit cards (requiring a cash deposit) may be the primary card option

- Higher auto insurance premiums

- Difficulty renting apartments in competitive markets

If your score is in this range, focus on identifying and disputing errors on your credit reports. Inaccuracies are more common than most people realize, and correcting them can produce quick score improvements. M1 Credit Solutions’ AI-powered dispute platform connects to all three bureaus and identifies negative items automatically.

VantageScore Ranges: How They Differ from FICO

VantageScore was created in 2006 by the three major credit bureaus (Experian, Equifax, and TransUnion) as a competitor to FICO. While VantageScore 3.0 and 4.0 use the same 300–850 credit score scale as FICO, the credit score ranges and factor weightings are different.

Here is the complete VantageScore credit score chart:

| VantageScore Range | Rating | Equivalent FICO Tier |

|---|---|---|

| 781–850 | Excellent | Exceptional / Very Good |

| 661–780 | Good | Good / Very Good |

| 601–660 | Fair | Fair |

| 500–600 | Poor | Poor / Fair |

| 300–499 | Very Poor | Poor |

Average VantageScore: The national average VantageScore is 700, placing the typical American in the “Good” tier, according to data from the three credit bureaus.

Why Your VantageScore and FICO Score Are Different

If you have ever checked your score on Credit Karma (which shows your VantageScore) and then seen a different number when a lender pulls your FICO score, you are not alone. A 20–40 point difference between the two models is completely normal. Here is why:

| Factor | FICO Score 8 | VantageScore 4.0 |

|---|---|---|

| Payment History | 35% | 41% |

| Credit Utilization | 30% | 20% |

| Length of Credit History | 15% | 20% |

| Credit Mix | 10% | 11% |

| New Credit / Inquiries | 10% | 6% |

| Available Credit | — | 2% |

Key differences:

- Minimum scoring requirements: FICO requires at least six months of credit history and at least one account reported in the past six months. VantageScore can generate a score with just one month of history, making it more accessible for people with thin credit files.

- Hard inquiry treatment: FICO deduplicates mortgage, auto, and student loan inquiries within a 45-day window. VantageScore uses a 14-day rolling window for all inquiry types.

- Collections handling: VantageScore 4.0 ignores paid collections entirely. FICO 9 also ignores paid collections, but the more widely used FICO 8 does not.

- Medical debt: VantageScore 4.0 excludes medical collections. FICO 9 excludes paid medical collections, but FICO 8 includes them.

FICO 8 vs. FICO 9 vs. FICO 10 vs. VantageScore 3.0: Model Comparison

Not all credit scores are created equal, even within the same brand. Lenders use different FICO versions depending on the product type. Understanding which model applies to your situation helps you interpret the score you see.

| Feature | FICO 8 | FICO 9 | FICO 10/10T | VantageScore 3.0 | VantageScore 4.0 |

|---|---|---|---|---|---|

| Score Range | 300–850 | 300–850 | 300–850 | 300–850 | 300–850 |

| Most Common Use | Credit cards, personal loans | Some lenders transitioning | Mortgages (transitioning) | Free monitoring apps | Some lenders, newer apps |

| Paid Collections | Counts against you | Ignored | Ignored (10T) | Ignored | Ignored |

| Medical Debt | Included | Paid collections excluded | Excluded (10T) | Excluded | Excluded |

| Rental Data | Not included | Included if reported | Included (10T) | Included if reported | Included if reported |

| Trended Data | No | No | Yes (10T) | No | Yes |

| Hard Inquiry Window | 45 days | 45 days | 45 days | 14 days | 14 days |

2026 Update: The Federal Housing Finance Agency (FHFA) has approved both FICO 10T and VantageScore 4.0 for Fannie Mae and Freddie Mac mortgage underwriting. This is the first time VantageScore has been approved for conventional mortgage lending. Full FICO 10T adoption is expected by Q4 2026, replacing the legacy FICO 2, 4, and 5 models that mortgage lenders have used for decades.

Which FICO Version Do Lenders Actually Use?

| Lending Product | Common FICO Version | Score Range |

|---|---|---|

| Mortgage | FICO 10T (transitioning from 2/4/5) | 300–850 |

| Credit Cards | FICO Bankcard Score 8 or FICO 8 | 250–900 / 300–850 |

| Auto Loans | FICO Auto Score 8 or Auto Score 9 | 250–900 |

| Personal Loans | FICO 8 or FICO 9 | 300–850 |

| Free Monitoring Apps | VantageScore 3.0 or 4.0 | 300–850 |

This is why the score you see on Credit Karma or your banking app can differ significantly from the score a lender pulls when you apply. They are literally different algorithms running against potentially different bureau data.

What Each Credit Score Tier Means for Real Lending Decisions

Your credit score tier directly impacts how much you pay for borrowed money. Here is a breakdown of what each range means for the most common financial products.

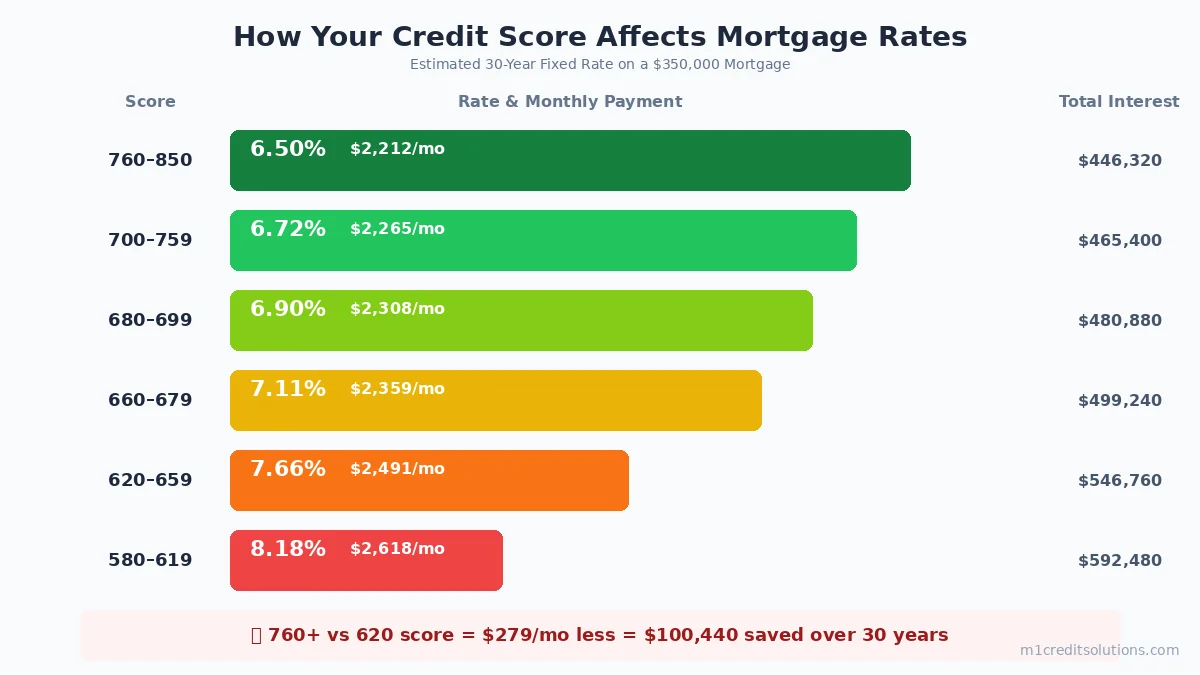

Mortgage Rates by Credit Score Range

Your credit score has the single biggest impact on your mortgage interest rate. Even a small difference in rate translates to tens of thousands of dollars over a 30-year loan.

| Credit Score Range | Estimated 30-Year Fixed Rate | Monthly Payment ($350K) | Total Interest Paid |

|---|---|---|---|

| 760–850 | 6.50% | $2,212 | $446,320 |

| 700–759 | 6.72% | $2,265 | $465,400 |

| 680–699 | 6.90% | $2,308 | $480,880 |

| 660–679 | 7.11% | $2,359 | $499,240 |

| 620–659 | 7.66% | $2,491 | $546,760 |

| 580–619 | 8.18% | $2,618 | $592,480 |

The bottom line: The difference between a 760+ score and a 620 score on a $350,000 mortgage is approximately $279 per month and over $100,000 in total interest over 30 years. That is the real cost of a lower credit score tier. For a deeper dive into what credit score you need to buy a house, see our dedicated guide.

Auto Loan Rates by Credit Score Range

| Credit Score Range | Estimated New Car APR | Estimated Used Car APR |

|---|---|---|

| 781–850 (Super Prime) | 5.6% | 7.4% |

| 661–780 (Prime) | 6.8% | 9.2% |

| 601–660 (Nonprime) | 9.5% | 13.2% |

| 501–600 (Subprime) | 12.8% | 17.6% |

| 300–500 (Deep Subprime) | 15.2%+ | 20.5%+ |

Credit Card Approval by Score Tier

| Score Tier | Card Types Available | Typical APR Range |

|---|---|---|

| 740+ (Excellent) | Premium travel, luxury, high-limit cashback | 16–21% |

| 670–739 (Good) | Mid-tier rewards, balance transfer | 19–25% |

| 580–669 (Fair) | Basic cards, some secured, higher fees | 24–29% |

| Below 580 (Poor) | Secured cards only (cash deposit required) | 26–30%+ |

Credit Score Needed for Major Life Events

Knowing what is a good credit score depends entirely on what you are trying to accomplish. Here is a practical breakdown of the minimum and ideal credit scores for major financial milestones.

| Life Event | Minimum Score | Recommended Score | Why It Matters |

|---|---|---|---|

| Buy a house (FHA) | 580 (500 with 10% down) | 680+ | Lower rates save $100K+ over the loan |

| Buy a house (Conventional) | 620 | 740+ | Best rates and lowest PMI costs |

| Buy a car (new) | No hard minimum | 700+ | Prime rates vs. subprime rates can differ by 8%+ |

| Rent an apartment | Varies by landlord | 650+ | Many landlords screen at 650 as a floor |

| Get a rewards credit card | 670+ | 740+ | Premium cards require excellent credit |

| Refinance a mortgage | 620 | 740+ | Only worth refinancing if you get a lower rate |

| Start a business (SBA loan) | 680+ | 720+ | Personal credit is checked for most SBA loans |

| Get the best insurance rates | No official minimum | 700+ | Many states allow credit-based insurance scoring |

For entrepreneurs working on both personal and business credit, understanding these thresholds is critical to unlocking financing at favorable terms.

How to Check Your Credit Score for Free

You can access your credit score from multiple free sources. Here are the most reliable options:

Free FICO Score Sources

- Experian app: Shows your official FICO Score 8 from Experian, updated monthly, at no cost

- Discover Credit Scorecard: Free FICO Score 8 from TransUnion, available to anyone (not just Discover cardholders)

- Many bank and credit card apps: Chase, Bank of America, Capital One, Citibank, and others provide free FICO scores to their customers

Free VantageScore Sources

- Credit Karma: Free VantageScore 3.0 from TransUnion and Equifax, updated weekly

- Credit Sesame: Free VantageScore 3.0 from TransUnion

- NerdWallet: Free VantageScore 3.0 from TransUnion

Free Credit Reports

- AnnualCreditReport.com: Free weekly reports from all three bureaus (Equifax, Experian, and TransUnion). This is the only federally authorized source.

- M1 Credit Solutions: Our credit score checking guide walks you through how to access and interpret your reports from all three bureaus.

Pro tip: Your credit report and your credit score are not the same thing. Your report contains the raw data (accounts, payments, inquiries). Your score is the number calculated from that data. Always check both, because errors on your report can drag down your score unnecessarily.

How to Move Up a Credit Score Tier

Moving up even one tier on the credit score chart can save you thousands of dollars. Here are the most effective strategies, ranked by impact.

Fastest Impact (30–90 Days)

- Dispute errors on your credit reports. Studies by the Federal Trade Commission found that 1 in 5 consumers had an error on at least one credit report. Errors like incorrect late payments, duplicate accounts, or wrong balances can drop your score by 50–100 points. Learn what affects your credit score and how to fix problems.

- Pay down credit card balances. Credit utilization (the percentage of your available credit you are using) accounts for 30% of your FICO score. Paying a card from 80% utilization to 30% can boost your score by 30–50 points in a single reporting cycle.

- Ask for a credit limit increase. If your income has increased, request higher limits on existing cards. This reduces your utilization ratio without requiring you to pay down balances.

- Become an authorized user. Being added to a family member’s old, low-utilization credit card can immediately add positive history to your profile.

- Set up autopay on every account. Payment history is 35% of your FICO score. Six months of on-time payments begins to outweigh past negative marks.

- Keep old accounts open. Even if you do not use a card, keeping it open maintains your credit history length (15% of FICO) and available credit (lowering utilization).

- Diversify your credit mix. If you only have credit cards, consider a credit-builder loan or a small installment loan. Credit mix accounts for 10% of your FICO score.

- Let negative items age off. Most negative items (late payments, collections, charge-offs) fall off your credit report after 7 years. Bankruptcies stay for 7–10 years.

- Build a track record. There is no substitute for years of on-time payments and responsible credit use. If your score is below 580, focus on the fundamentals and give yourself 12–24 months to build a foundation.

- Highest: Minnesota (742), Vermont (737), Wisconsin (737)

- Lowest: Mississippi (691), Louisiana (695), Alabama (697)

- National gap: 51 points between the highest and lowest state averages

Medium-Term Impact (3–12 Months)

Long-Term Impact (12+ Months)

If you need help identifying the specific items pulling your score down, M1 Credit Solutions’ AI-powered DIY credit repair platform connects to all three bureaus, scans your reports automatically, and generates custom dispute letters tailored to your situation. Learn how to improve your credit score fast with a structured, step-by-step approach.

Credit Score Distribution in America: Where Do You Stand?

Understanding where your score falls relative to other Americans provides useful context. Here is the current distribution of FICO scores across the U.S. population:

| FICO Score Tier | Score Range | % of Population | Cumulative % |

|---|---|---|---|

| Exceptional | 800–850 | 24% | 24% |

| Very Good | 740–799 | 17% | 41% |

| Good | 670–739 | 21% | 62% |

| Fair | 580–669 | 18% | 80% |

| Poor | 300–579 | 16% | 96% |

| No Score | N/A | ~4% | 100% |

Average Credit Score by Generation

Credit scores tend to increase with age as credit histories grow longer and consumers develop better financial habits.

| Generation | Average FICO Score (2025) | Credit Tier |

|---|---|---|

| Silent Generation (78+) | 760 | Very Good |

| Baby Boomers (61–77) | 745 | Very Good |

| Gen X (45–60) | 709 | Good |

| Millennials (29–44) | 696 | Good |

| Gen Z (18–28) | 680 | Good |

Average Credit Score by State

The geographic credit score gap in the United States is significant. Upper Midwest and New England states consistently rank highest, while Southeastern states trail.

Frequently Asked Questions

What is the highest possible credit score?

The highest possible credit score is 850 on both the FICO and VantageScore (3.0 and 4.0) scales. As of 2025, approximately 1.7% of Americans have a perfect 850 FICO score. While an 850 is impressive, the practical benefits plateau around 760–780. Once you reach that range, you already qualify for the best rates on virtually every credit product.

Is 700 a good credit score?

Yes. A 700 credit score falls in the “Good” tier on the FICO scale (670–739). You will qualify for most mainstream credit products, including conventional mortgages, auto loans, and mid-tier credit cards. However, moving up to 740+ (“Very Good”) unlocks better interest rates and premium card options.

What credit score do you need to buy a house?

The minimum depends on the loan type. FHA loans require a 580 score for 3.5% down (or 500 with 10% down). Conventional loans typically require 620+. VA loans have no official minimum, but most lenders want 580–620. For the best mortgage rates, aim for 740+. Read our complete guide on credit scores needed to buy a house.

How often does my credit score change?

Your credit score can change every time new information is reported to the credit bureaus, which typically happens monthly. When a lender or creditor reports an updated balance, a new account, or a missed payment, your score is recalculated. You are not assigned a static number; the score is generated fresh each time it is requested.

Why is my Credit Karma score different from my FICO score?

Credit Karma shows your VantageScore 3.0 from TransUnion and Equifax. Most lenders use FICO scores. The two models use different algorithms and weight credit factors differently. A 20–40 point difference between your VantageScore and FICO score is completely normal and does not indicate an error.

What is the fastest way to raise my credit score?

The fastest methods are disputing errors on your credit reports (which can produce results in 30–45 days) and paying down high credit card balances (which is reflected in your score within one billing cycle, typically 30 days). For a step-by-step approach, check our guide on how to improve your credit score fast.

Does checking my own credit score lower it?

No. Checking your own credit score is a “soft inquiry” and does not affect your score in any way. You can check as often as you want without any negative impact. Only “hard inquiries” from lenders when you apply for credit can temporarily lower your score by a few points.

What is the difference between a credit score and a credit report?

Your credit report is the detailed record of your credit history, including all your accounts, payment records, balances, and inquiries. Your credit score is a three-digit number calculated from the data in your credit report. Think of the report as the raw data and the score as the summary. You can get your free credit report from AnnualCreditReport.com.