Business Line of Credit vs. Business Loan: Which Is Right for Your Company?

Choosing between a business line of credit vs business loan can shape how confidently your company handles cash flow, growth, and unexpected expenses. Both options can help you access capital, but they work differently. A line of credit gives you flexible access to funds as needed, while a business loan delivers a lump sum for a defined purpose.

Need funding without guessing which lender fits? Get matched with a business lender in minutes through M1 Credit Solutions and compare options based on your needs, credit profile, and business stage.

The right choice depends on why you need money, how quickly you plan to repay it, and whether your cash needs are ongoing or one time. This guide compares how each product works, typical rates and repayment terms, qualification requirements, pros and cons, and a practical decision framework for small business owners.

As you compare financing options, review your business credit reporting agencies profiles too, because lenders and vendors may use those records to judge repayment risk.

Business Line of Credit vs Business Loan: Quick Comparison

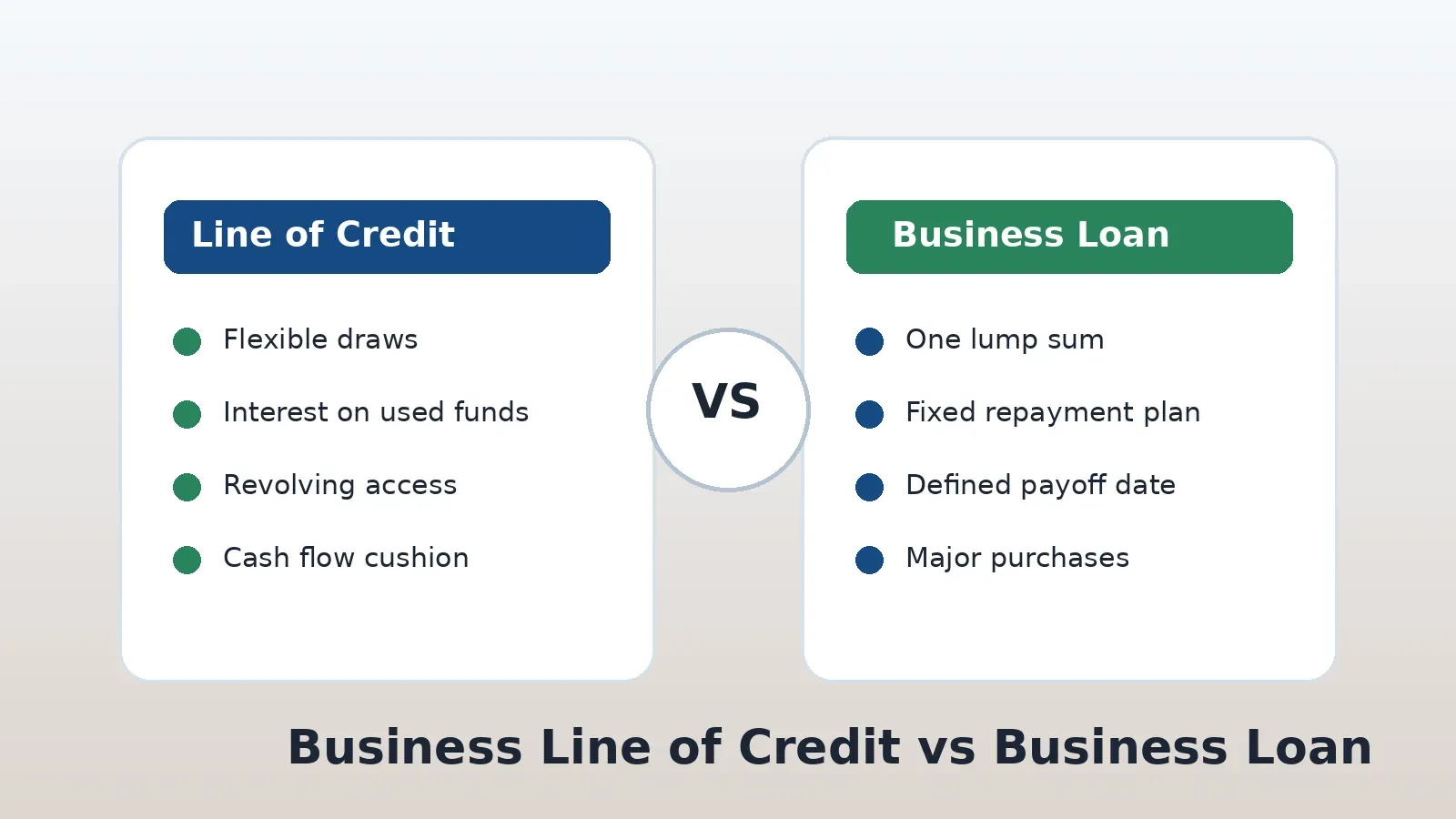

At a high level, the difference comes down to flexibility versus structure. A business line of credit is revolving. You can draw, repay, and draw again up to your approved limit. A business loan is installment based. You receive one lump sum and repay it over a set term.

| Feature | Business Line of Credit | Business Loan |

|---|---|---|

| Funding structure | Revolving credit limit | One lump sum |

| Best for | Recurring expenses, cash flow gaps, seasonal needs, emergencies | Equipment, expansion, large purchases, refinancing, major projects |

| Interest charged on | Only the amount you draw | The full loan balance after funds are issued |

| Repayment style | Repay each draw, often weekly or monthly | Fixed payments over a set term |

| Typical terms | Often shorter terms for each draw, commonly months to a few years | Can range from months to several years, depending on product and lender |

| Funding amount | Usually lower than large term loans | Often better for larger capital needs |

| Flexibility | High | Moderate to low after funding |

| Predictability | Depends on usage | High, especially with fixed payments |

How Does a Business Line of Credit Work?

A business line of credit gives your company access to a maximum credit limit, such as $10,000, $50,000, or more. You do not have to use the entire amount. If you draw $8,000 from a $50,000 line, you typically pay interest only on the $8,000 you used, not the full $50,000 limit.

As you repay the balance, your available credit can replenish. That revolving structure makes a line of credit useful for expenses that come in waves, including inventory purchases, payroll timing gaps, repair bills, vendor deposits, or slow customer payments.

Example of a line of credit in action

Imagine a landscaping company with a $40,000 business line of credit. In March, the owner draws $12,000 for seasonal supplies and payroll before customer payments begin. By May, invoices are paid and the business repays the draw. In July, a truck repair creates a $6,000 expense, and the owner draws again. The company uses funding only when needed instead of taking a large loan upfront.

When a line of credit makes sense

- You have recurring or unpredictable cash flow needs.

- You want a funding cushion available before an emergency happens.

- You need to buy inventory before revenue comes in.

- You want to avoid paying interest on unused capital.

- You may need smaller draws over time instead of one large amount.

How a Business Loan Works

A business loan provides a specific amount of capital upfront. Once approved, the lender sends the funds to your business, and you repay the balance over a set period with interest and any applicable fees. Business loans may include term loans, equipment financing, SBA loans, working capital loans, and other structured financing options.

Because the funds are issued as a lump sum, business loans are often best when you know the cost of the project or purchase. If you need $80,000 for equipment, renovation, a vehicle, or a planned expansion, a term loan can give you a clear repayment schedule and defined payoff date.

Example of a business loan in action

A restaurant owner needs $75,000 to remodel the dining room and upgrade kitchen equipment. The project has a clear budget, timeline, and expected return. A business loan may be a better fit than a line of credit because the owner needs the full amount at once and wants predictable payments over time.

When a business loan makes sense

- You need a larger amount of capital for a defined purpose.

- You want predictable payments and a clear payoff schedule.

- You are investing in equipment, expansion, renovation, or acquisition.

- You do not need to borrow repeatedly after the first funding event.

- You can match the repayment term to the useful life of the investment.

Which Costs Less: a Line of Credit or Business Loan?

Rates and terms vary widely by lender, product type, credit profile, revenue, time in business, collateral, and overall risk. Online lenders may move faster and approve a wider range of credit profiles, but they can charge higher rates or shorter terms. Banks and SBA-backed lenders may offer stronger terms, but approval standards are often stricter.

Business line of credit rates and repayment

With a line of credit, the cost is tied to your usage. You may receive an approved limit, but interest usually begins only when you draw funds. Some lenders charge draw fees, maintenance fees, or origination fees, so it is important to compare the total cost, not just the stated rate.

Repayment may be weekly or monthly. Short-term online lines may require faster repayment on each draw, while bank lines may offer longer repayment windows. Because the balance can change as you draw and repay, your payment amount may be less predictable than a fixed term loan.

Business loan rates and repayment

With a business loan, you typically start paying interest after receiving the lump sum. Many term loans use a fixed payment schedule, which makes budgeting easier. Repayment may range from several months for short-term working capital loans to multiple years for equipment, SBA, or bank financing.

A loan can be more cost effective than a line of credit when the borrower has strong qualifications and a clear use for the funds. However, if you borrow more than you need, you may pay interest on capital that sits unused.

Is a Business Line of Credit Easier to Qualify For?

Lenders look at risk from several angles. The stronger your credit, revenue, and business history, the more options you may have. Requirements differ by lender, but most review the following factors.

Credit score

Your personal credit score can matter, especially for newer or smaller businesses. Business owners with stronger credit may qualify for lower rates, larger amounts, and longer repayment terms. Owners with lower credit may still have options through alternative lenders, secured products, revenue-based products, or specialized funding programs, but the costs may be higher.

If personal credit is holding your business back, M1 Credit Solutions offers resources to help you understand and improve credit health. Start with how to improve your credit score and how better credit can improve loan options.

Time in business

Many lenders prefer businesses with at least six months to two years of operating history. Startups can still qualify for certain products, but they may face lower limits, higher rates, personal guarantees, or additional documentation requirements.

Revenue and cash flow

Lenders want to see that your business can repay. They may review monthly revenue, bank statements, profit trends, existing debt payments, and cash flow consistency. A business with strong revenue but seasonal swings may prefer a line of credit, while a business with stable cash flow may handle a fixed loan payment more comfortably.

Business credit profile

A separate business credit profile can help your company look more established and may reduce reliance on personal credit over time. If your business credit is thin, read M1’s guide on how to build business credit before applying for larger funding.

Collateral and guarantees

Some loans or lines of credit are secured by equipment, inventory, receivables, or other assets. Others may be unsecured but still require a personal guarantee. Unsecured lines can be convenient, but they may come with lower limits or higher rates. For more detail, see M1’s guide to a business line of credit with no collateral.

Pros and Cons of a Business Line of Credit

Pros

- Flexible access: Draw what you need, when you need it.

- Interest on used funds: You generally pay interest only on the amount drawn.

- Reusable capital: As you repay, available credit can replenish.

- Strong cash flow tool: Helpful for seasonal businesses, inventory cycles, and short-term gaps.

- Emergency cushion: Can be available before a crisis hits.

Cons

- Variable cost: Payments and interest can change based on usage and terms.

- Possible fees: Some lenders charge draw, maintenance, or inactivity fees.

- Lower limits: May not be ideal for large purchases or major expansion.

- Shorter repayment windows: Some online lines require fast repayment after each draw.

- Discipline required: Easy access can lead to borrowing for nonessential expenses.

Pros and Cons of a Business Loan

Pros

- Large upfront funding: Useful for major purchases, equipment, renovations, or expansion.

- Predictable payments: Fixed schedules make planning easier.

- Defined payoff date: You know when the debt should be repaid.

- Potentially longer terms: Strong borrowers may qualify for multi-year repayment.

- Strategic investment: Works well when capital is tied to a specific growth project.

Cons

- Less flexible: If you need more money later, you may need another application.

- Interest on full amount: You pay for the entire balance, even if some funds are unused.

- Stricter approval: Larger loans may require stronger credit, revenue, collateral, or documentation.

- Potential prepayment rules: Some lenders charge fees or limit savings if you repay early.

- Debt burden: A large fixed payment can pressure cash flow if revenue slows.

Which Option Is Better for Your Use Case?

The best financing choice depends on the job you need the money to do. Start with the purpose of the funds, then match that purpose to the repayment structure.

Choose a business line of credit if you need revolving working capital

A line of credit is often the better fit for cash flow timing issues, short-term operating expenses, inventory cycles, and emergency reserves. It gives you access without forcing you to borrow the full limit upfront.

Mid-article funding check: If you are not sure which product your business can qualify for, use M1 Credit Solutions to get matched with a lender in minutes. Matching can help you compare available options without starting from scratch with every lender.

Choose a business loan if you need one-time capital

A business loan is often the better fit when you know the amount, cost, and purpose. Equipment, buildouts, major marketing campaigns, acquisitions, and long-term expansion plans usually benefit from structured repayment.

Consider using both strategically

Some businesses use a loan and a line of credit for different purposes. For example, a company might use a term loan to buy equipment and a line of credit to manage payroll during seasonal slow periods. The key is avoiding overlapping debt that strains cash flow.

A Simple Decision Framework for Small Business Owners

Use these questions before applying.

- Is the expense one time or recurring? One-time needs often point to a loan. Recurring needs often point to a line of credit.

- Do you know the exact amount you need? If yes, a loan may fit. If no, flexible credit may be safer.

- Will the funding create measurable return? Match repayment to expected revenue or savings.

- Can your cash flow support fixed payments? If not, a line may provide more breathing room, but only if used carefully.

- How strong are your qualifications? Review credit score, time in business, revenue, and business credit before applying.

- What is the total cost? Compare interest, fees, repayment frequency, prepayment rules, and required guarantees.

If the money supports a defined growth move, a business loan may be right. If the money protects day-to-day operations, a business line of credit may be right. If your credit profile limits your options, focus on lender matching and credit preparation before accepting expensive terms.

How to Prepare Before You Apply

Whether you choose a business line of credit or a business loan, preparation can improve your odds and help you avoid poor-fit offers.

- Review personal and business credit reports for errors or outdated information.

- Gather recent bank statements, tax returns, profit and loss statements, and debt schedules.

- Calculate how much you actually need and how repayment fits your cash flow.

- Separate personal and business finances as much as possible.

- Build or strengthen your business credit profile before seeking larger funding.

- Compare multiple lenders instead of accepting the first offer.

M1 Credit Solutions helps small business owners think through both sides of the funding equation: finding lender options and building stronger credit foundations. Explore business loan matching resources and the guide to building business credit if your company is preparing for funding.

Bottom Line: Match the Financing to the Job

When comparing a business line of credit vs business loan, do not start with which option sounds easier. Start with the job the money needs to do. A line of credit is usually better for flexible, recurring, or unpredictable needs. A business loan is usually better for a planned investment with a known cost and a longer repayment horizon.

Both products can be useful when used for the right purpose. The smarter move is to compare lenders, understand the total cost, and choose financing that supports growth without creating unnecessary pressure on your cash flow.

Ready to compare business funding options? Get matched with a lender in minutes through M1 Credit Solutions and take the next step toward the capital your company needs.

FAQ

Is a business line of credit the same as a business loan?

No. A business line of credit is revolving, so you can draw funds as needed up to a limit. A business loan provides one lump sum that you repay over a set term.

Is it easier to qualify for a business line of credit or a loan?

It depends on the lender and product. Some online lines of credit may be more accessible for newer businesses or lower credit profiles, while larger term loans often require stronger credit, revenue, and time in business.

Which is cheaper, a business line of credit or a business loan?

A business loan may be cheaper for a qualified borrower with a clear one-time need. A line of credit may cost less when you only need to use a small portion of your approved limit because interest is usually charged only on the amount drawn.

Can I use a business line of credit for equipment?

You can, but it may not always be the best fit. If the equipment is expensive and will be used for years, equipment financing or a term loan may offer a better repayment structure.

Can I have both a business loan and a line of credit?

Yes. Many businesses use both for different purposes. A loan can fund a major purchase, while a line of credit can support working capital. The important step is making sure total debt payments fit your cash flow.